What to Do If A Reversal Takes More Than 24 Hours

Whether you attempted a withdrawal at an ATM only to see your account debited without cash, or a payment via POS or online transfer failed but your account still shows the amount deducted, most Nigerians have faced the same unsettling scenario: the reversal doesn’t happen as quickly as expected.

You were told the refund would arrive within hours. It didn’t. And now you’re wondering: What next?

This article explains, step-by-step, what you should do when that reversal takes longer than 24 hours including timelines, documentation, escalation routes, and your rights as a bank customer.

Understanding Expected Reversal Timelines

First, let’s briefly explain what the rule is because if a reversal takes longer than expected, you should know what the standard should be.

In Nigeria, the Central Bank of Nigeria (CBN) has long issued guidelines requiring banks to process failed ATM reversals quickly:

For “on us” ATM transactions (when you use your own bank’s ATM), the reversal should be instant, or within 24 hours if instant reversal fails due to technical issues.

For “not on us” ATM transactions (when you use another bank’s ATM), refunds should be completed within 48 hours.

For disputed or failed POS or web/electronic transactions, the timelines are also capped (often within 72 hours

More recently, new draft guidelines from the CBN reinforce this requirement and explicitly state that banks must automatically reconcile and refund failed or partial transactions without customers having to lodge a complaint.

So when your reversal exceeds these timelines, something has gone wrong and it’s reasonable to take action.

Why a Reversal May Take Longer Than Expected

A delay doesn’t always mean negligence. There are several common reasons a bank may not immediately process a refund:

- Network Glitches: Banks rely on large, interconnected systems (NIBSS, internal core banking systems, ATM switches). A network glitch between any of these can delay automated reversal processes.

- Interbank Settlement Differences: If the failed transaction involved interbank communication as in ATM or transfer across banks reconciliation between systems can take longer than perfectly in bank cases.

- Manual Investigation:In rare cases where a bank flags a discrepancy (for example, the terminal reported success but the host bank shows no record), the reversal may be held for manual validation by a bank officer.

- Peak Load Periods: Weekends, holidays, and end of month spikes in transactions add load to systems, slowing down automated processes an informal but real factor in the Nigerian banking context.

Knowing why delays happen can be reassuring but it doesn’t mean waiting indefinitely.p

Step-by-Step Guide: What You Should Do

Here is a practical, actionable pathway to follow when a reversal hasn’t posted within 24 hours:

- Confirm the Reversal Status:

Before doing anything else, make sure the reversal really hasn’t occurred:

- Check your bank app or mobile banking

- Use USSD balance and transaction history

- Review SMS notifications

Sometimes reversals post quietly without push notifications. If a debit is still shown, proceed to the next step.

- Gather Your Evidence :

A successful complaint and faster resolution depends on good documentation. Make sure you have:

- Transaction reference number

- Screenshot of the debit alert or bank statement

- Time and date of the transaction

- Any receipt or message from the ATM, POS, or app

These details are critical when you formally report the case to your bank or escalate beyond that.

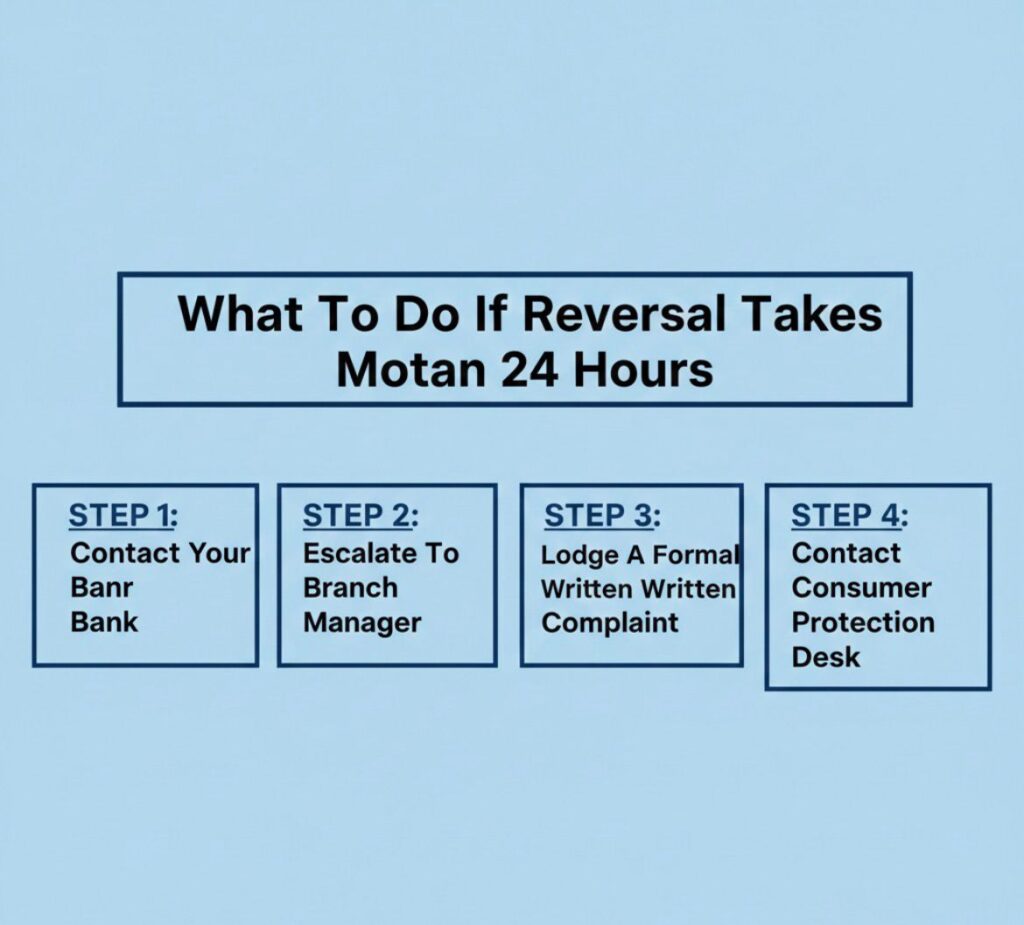

- Contact Your Bank Promptly

Begin with your bank’s official support channels. You can do this in multiple ways:

- In app Support / Live Chat : Many banks now integrate support directly into mobile apps use this because it creates a digital thread of your complaint.

- Call the Customer Care Line Have your transaction details ready. Ask for a complaint reference number so you can track follow ups.

- Visit a Branch Especially if you made an ATM transaction, visiting a branch allows you to log a dispute at the help desk with printed records.

When you speak to support, clearly state:

- “My reversal was due in 24/48 hours (as per CBN guidelines), but it’s still not reflected. Please escalate and confirm the status.”

- Track the Complaint and Follow Up

Banks often promise to update you within a set period (e.g., 48 hours). If this period expires:

Follow up frequently with your reference number.

Ask for status updates in writing via email or SMS.

Keep all communication saved.

In many cases, persistent follow-up nudges the bank’s internal investigation, especially if the issue is due to manual validation.

- Escalate to the CBN Consumer Protection Desk (If Needed)

If your bank fails to resolve the issue within a reasonable time after you’ve followed their dispute process, you can escalate to the Central Bank of Nigeria’s Consumer Protection Department (CPD).

While the CBN doesn’t directly intervene in every case, they can put official pressure on a bank to comply with regulatory timelines especially if the bank is found to be holding funds beyond the stipulated reversal window.

When escalating, prepare:

- Your correspondence with the bank

- Screenshots and transaction evidence

- Complaint reference numbers

Document everything clearly the more precise your submission, the faster the regulator can respond.

Avoid Common Mistakes

While you pursue resolution, don’t fall into these traps:

- Don’t re initiate the same transaction before confirming reversal this risks duplicate charges.

- Don’t rely on verbal promises without written confirmation.

- Don’t delete transaction screenshots or alerts they are essential proof.

Taking these precautions protects you from further headaches.

A Broader Perspective: Customer Rights and Bank Obligations

The push for quick reversal timelines isn’t just about convenience it’s about fairness in the financial system. The CBN’s 2020 revised guidelines on electronic payment channels explicitly instruct banks to:

- Immediately reverse failed on-us ATM transactions, with a 24 hour fallback if instant reversal fails.

- Complete not on us ATM refunds within 48 hours.

- Treat POS and web transaction reversals with similarly tight windows.

And in 2025 the CBN’s draft ATM operation guidelines reinforced these principles by requiring banks and ATM operators to put in place systems that automatically handle reversals without customer prompting.

These rules exist for one main reason: you should not bear the cost of technical failures beyond a very short, defined window.

Conclusion

Persistence Works, Backed By Regulation

When a bank reversal does not show up within the expected 24-48 hours, it’s normal to feel frustrated. But understanding the timelines, your rights, and the step-by-step actions you can take from documenting evidence, reporting to your bank, tracking your complaint, and escalating to the CBN if necessary gives you agency.

Remember:

Banks must reverse failed transactions within prescribed timelines.

Documentation and follow up are your strongest tools.

Regulators have made these expectations clear and they expect banks to honour them.

Handled well, what starts as a stressful situation can end with your funds safely returned and with a better understanding of how the financial system protects you.

Comments