Penalty for Late Income Tax Payment in Nigeria

Meeting tax deadlines isn’t just a good habit it’s a legal obligation in Nigeria. Whether you’re an individual taxpayer, a sole trader, or a business owner, the consequences of failing to pay your income tax on time can be costly and far-reaching.

Understanding these penalties is crucial not only to avoid extra charges but also to safeguard your financial reputation, business opportunities, and legal standing in Nigeria.

Why Timely Payment Matters

Income tax laws in Nigeria particularly the Companies Income Tax Act (CITA) and the Personal Income Tax Act (PITA) set clear deadlines for settlement of tax liabilities. When taxes aren’t paid on time:

- Penalties are charged

- Interest accrues on outstanding balances

- Legal and administrative actions may follow

This framework ensures fairness in the tax system and supports government revenue collection for public services.

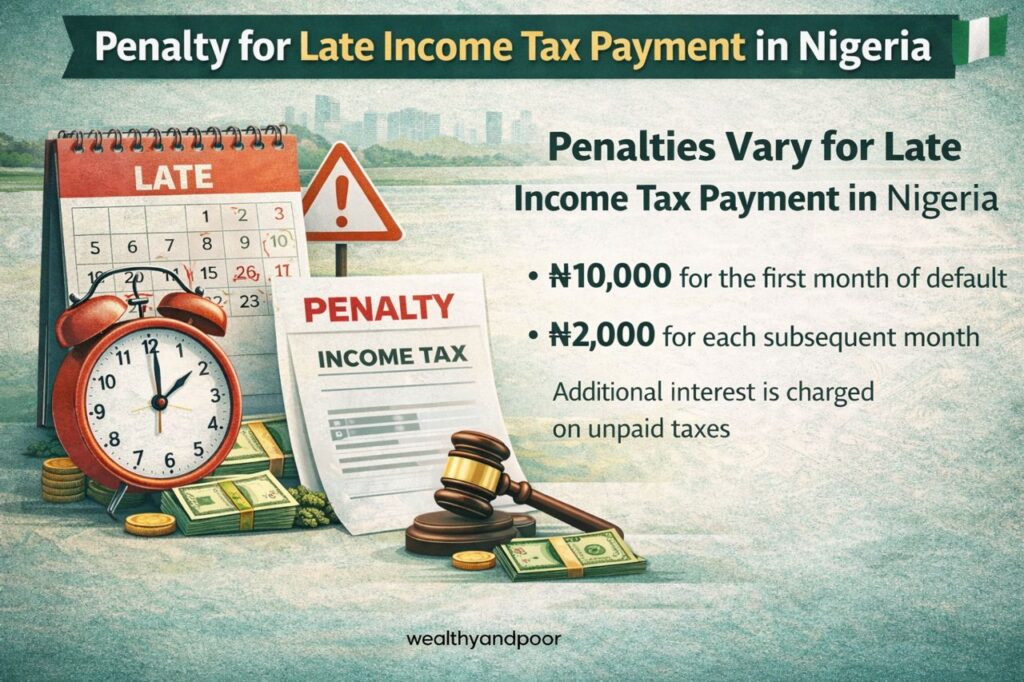

How Penalties for Late Payment Are Calculated

- Fixed Penalty + Interest

The most fundamental penalty for late payment of income tax in Nigeria is a surcharge on the unpaid amount, coupled with interest from the due date until full payment:

Surcharge: 10% of the outstanding tax due

Interest: Charged at the Central Bank of Nigeria (CBN) Monetary Policy Rate (MPR) plus any spread set by the Minister of Finance

Both surcharge and interest continue to accrue until the taxpayer makes full payment.

This means if you owe tax and you miss the deadline, you don’t just pay what you owe you pay more. The longer you delay, the more expensive it becomes.

For example, if a business owes ₦1,000,000 and fails to pay on time, a 10% penalty alone adds ₦100,000, and interest will keep accumulating from the original due date.

Penalties Across Different Tax Types

Here’s a breakdown of how late payment penalties work across common tax categories:

- Companies’ Income Tax (CIT)

Deadline: Within six months after the financial year-end (for most companies)

Late payment penalty:

10% of unpaid tax

Interest at CBN’s prevailing rate from the due date until payment.

- Personal Income Tax (PIT)

Deadline: Usually March 31 for individuals

Employer PAYE obligations: Monthly payments are due by the 10th of the following month

Late payment consequences:

Employers who fail to remit PAYE may attract a 10% penalty of the tax not remitted plus interest.

- Withholding Tax (WHT)

Payment due: By the 21st day of the month following deduction

Penalty: 10% of amount not remitted plus interest at prevailing rates.

Non-Financial Consequences of Late Payment

Penalties aren’t only financial. Failing to pay tax on time can hurt you in other significant ways:

- Tax Clearance Certificate (TCC) Withheld

A Tax Clearance Certificate is often required to:

- Bid for government contracts

- Apply for visas

- Obtain loans or credit

Failing to pay taxes can lead to refusal of this important document.

- Banking & Transaction Issues

Under modern enforcement approaches, the tax authority can flag non-compliant taxpayer records, which may affect banking operations or major financial transactions.

- Legal Enforcement

In extreme cases especially where deliberate evasion or fraud is suspected the law allows:

- Court summons

- Civil recovery of owed taxes

- Possible criminal prosecution

- Asset seizure to settle outstanding tax debts.

These outcomes are rare for honest mistakes but can happen with persistent or intentional default.

Best Practice Tips to Avoid Penalties

Here are some practical steps taxpayers in Nigeria should follow to avoid late payment penalties:

- Mark Your Tax Calendar

- Income tax deadlines vary:

Corporation tax: Within six months after year-end

Individual tax: Usually by March 31

PAYE: Monthly by the 10th

WHT: Monthly by the 21st

Always confirm specific dates with your tax professional or tax authority.

- Pay What You Can on Time

Even partial payments can reduce interest and penalty accumulation until the balance is settled.

- File Even if You Can’t Pay

Filing returns on time even without payment helps demonstrate compliance and avoids separate late-filing penalties. The penalty for late filing is different from the penalty for late payment so stay ahead on both.

- Seek Professional Help

Tax laws change frequently. If you’re unsure about deadlines or how penalties apply to your situation, consult a tax advisor.

Conclusion

Tax obligations might feel tedious, but they’re part of the social contract that keeps government functions running. Paying your income tax on time protects your finances, your business, and your legal standing. And if you can’t pay by the due date, it’s far cheaper to address the liability promptly than to let penalties and interest snowball.

Comments