How to Pay Tax for Small Business in Nigeria

Why Tax Matters for Your Business

Paying taxes is more than just a legal obligation it’s a key part of running a legitimate, sustainable business in Nigeria. Compliance helps you:

- Avoid penalties and legal issues

- Build credibility with clients and banks

- Qualify for government contracts and opportunities

- Access financing or grants that require tax clearance

Nigeria’s tax system operates on a self-assessment basis, meaning you assess, file, and pay most taxes yourself through the appropriate system and authorities.

Register Your Business for Tax

Before you can pay any tax, you must register your business and obtain a Tax Identification Number (TIN):

Step-by-Step

- Register your business with CAC (Corporate Affairs Commission) whether as a sole proprietor, partnership, or limited company.

- Apply for your TIN from the Federal Inland Revenue Service (FIRS) or your State Internal Revenue Service (if you operate as a sole proprietor).

The TIN is compulsory for all tax filings, opening business bank accounts, and official business operations.

Note: Without a TIN, you cannot legally file returns or pay taxes.

Know the Taxes Your Business May Pay

Understanding which taxes apply to you depends on your business type, revenue level, and workforce. Below are the common ones.

- Company Income Tax (CIT)

Charged on profit of companies incorporated in Nigeria.

Small businesses with turnover under ₦25 million are usually exempt from CIT.

Typical CIT rates (approx.):

- Business Size

- Turnover

- CIT Rate

Small < ₦25m ( 0%)

Medium <₦25m– ₦100m ( 20% )

Large > ₦100m ( 30% )

CIT returns are filed annually and must be submitted within six months after the company’s financial year end.

- Personal Income Tax (PIT)

If your business is sole proprietorship or partnership, your business income is taxed as personal income.

Tax rates are graduated meaning higher income attracts higher tax.

Businesses with employees must deduct PAYE (Pay-As-You-Earn) from salaries and remit monthly to the State IRS.

- Value Added Tax (VAT)

VAT is a consumption tax charged on the sale of goods and services.

Current VAT rate in Nigeria: 7.5%.

You collect VAT from customers and remit to FIRS monthly, usually by the 21st day of the next month.

If your annual turnover is below a certain threshold (often ₦25–50 million), you may file NIL returns until you exceed it.

- Withholding Tax (WHT)

Withholding Tax is deducted at the source on certain payments, such as:

- Rent

- Professional and contractor fees

- Consultancy and service charges

Rates vary (commonly 5%–10%) and must be remitted to tax authorities within a specified period (often within 21 days).

- Other Taxes and Levies

Depending on your activity and structure, you may also encounter:

- Business Premises Tax – a state levy for operating a business property.

- Capital Gains Tax — on gains from selling business assets.

- Stamp Duties — on legal documents and agreements.

- Education Tax (TETFund) — a levy on assessable profits for companies subject to CIT.

Filing Frequency & Deadlines

Tax Type. Filing Frequency. Due Date

CIT. Annual. Within 6 months after financial year end

VAT. Monthly. 21st of following month

PAYE. Monthly. Usually 10th of following month

WHT. Monthly. Within ~21 days of deduction

Missing deadlines can lead to fines, interests, or penalties.

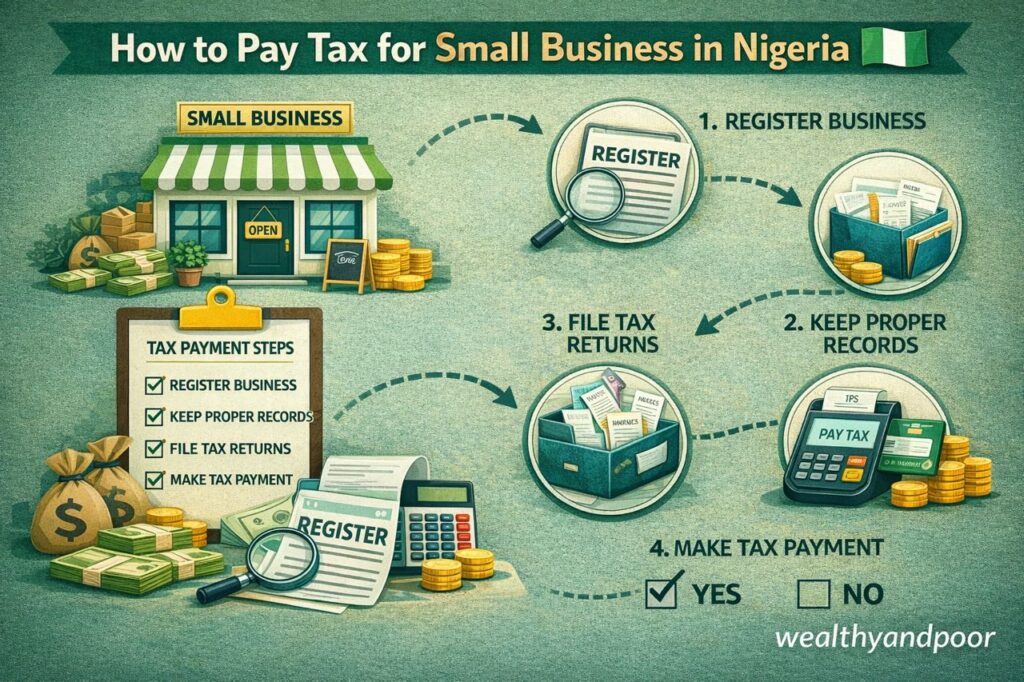

Simple Workflow for Paying Taxes

Step-by-Step Process

- Get your TIN — from FIRS or your state tax authority.

- Identify applicable taxes — based on business structure and turnover.

- Keep accurate records — income, expenses, employee pay, invoices.

- Calculate tax liabilities — using accounting software or a tax consultant.

- File returns on time — monthly or annually as required.

- Make payments — through designated bank channels or online portals.

- Keep proof of payment — for audits and compliance.

Tools for Compliance

- FIRS Tax pro max portal — for filing and payments online.

- Professional tax consultants or accountants — highly useful for accuracy.

- Accounting software (QuickBooks, Excel, or local fintech tools) to manage books and generate reports.

Conclusion

Stay updated on tax laws — they change often.

Separate business and personal accounts.

Don’t ignore small liabilities — minor unpaid taxes can become significant penalties.

Engage a professional if you’re unsure.

Comments