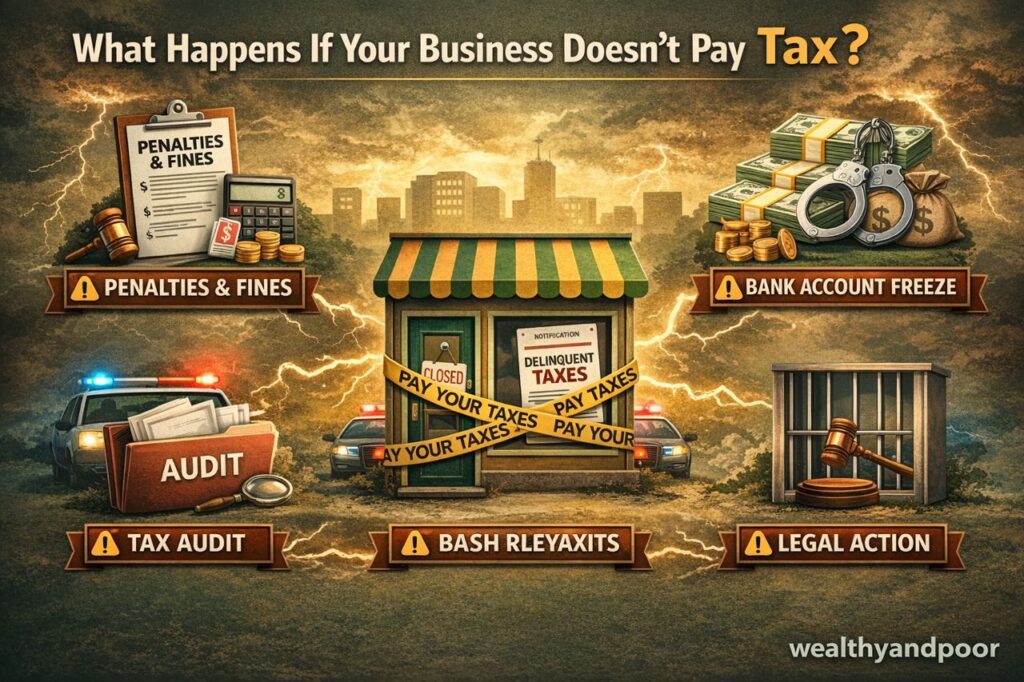

What Happens If Your Business Doesn’t Pay Tax?

For many small and growing businesses, especially in Nigeria’s informal and semi-formal sectors, tax compliance often takes a back seat to survival. Cash flow pressures, unstable exchange rates, regulatory bottlenecks, and rising operating costs can make tax obligations feel secondary.

But failing to pay tax is not a minor administrative issue. It can trigger financial penalties, legal consequences, reputational damage, and in extreme cases, business closure.

This article explains what really happens when a business does not pay tax with a focus on Nigeria and why compliance is no longer optional in today’s increasingly digitised tax environment.

Immediate Financial Penalties and Interest

The first and most predictable consequence of not paying tax is financial penalties.

In Nigeria, taxes are administered by the Federal Inland Revenue Service (FIRS) and various State Internal Revenue Services. The legal framework is largely governed by the Companies Income Tax Act (CITA), the Federal Inland Revenue Service (Establishment) Act, and the Personal Income Tax Act (PITA).

Under the Companies Income Tax Act:

- Failure to file returns attracts penalties starting from ₦25,000 for the first month and ₦5,000 for each subsequent month of default.

- Failure to pay tax when due attracts interest at the prevailing Central Bank of Nigeria minimum rediscount rate plus a spread.

Over time, these penalties compound. A business that originally owed ₦5 million could find its liability significantly higher within a year due to accumulated interest and fines.

Tax Audits and Investigations

Non-payment often triggers tax audits.

The Federal Inland Revenue Service (FIRS) has significantly increased its audit activities in recent years, particularly as Nigeria seeks to improve its tax-to-GDP ratio.

When flagged:

- Your business accounts may be reviewed.

- Bank records may be scrutinised.

- Transaction histories can be requested.

- Third-party information (customers, suppliers, financial institutions) may be examined.

- If discrepancies are found, the tax authority may issue additional assessments sometimes covering multiple prior years.

With digital banking records and improved inter-agency data sharing, hiding revenue is far more difficult today than it was a decade ago.

Freezing of Bank Accounts

One of the most serious consequences is the freezing of business bank accounts.

In the past few years, tax authorities have obtained court orders to place liens on accounts of companies with outstanding tax liabilities. Once frozen:

- The business cannot withdraw funds.

- Salary payments may be disrupted.

- Suppliers may not be paid.

- Daily operations can stall.

For small businesses operating on tight margins, this can be devastating.

Even if the dispute is later resolved, the operational damage may already be done.

Legal Action and Prosecution

Persistent non-compliance can escalate to litigation.

Under Nigerian tax laws, tax evasion especially deliberate falsification of records or concealment of income is a criminal offence.

Consequences may include:

- Court summons

- Seizure of assets

- Fines

- In severe cases, imprisonment of company directors

While imprisonment is rare and usually reserved for extreme cases, the reputational and legal costs of prosecution are significant.

For directors, tax offences can also affect eligibility to hold corporate positions in the future.

Loss of Government Contracts and Business Opportunities

Increasingly, tax compliance is tied to eligibility for contracts and financial opportunities.

To bid for many government contracts in Nigeria, a business must provide a valid Tax Clearance Certificate (TCC). Without evidence of tax compliance:

- You may be disqualified from public tenders.

- Grants and funding opportunities may become inaccessible.

- Partnerships with multinationals may be affected.

Banks and investors also conduct tax due diligence. Outstanding tax liabilities can derail funding rounds, acquisitions, or expansion plans.

In short, tax non-compliance limits growth.

Reputational Damage

In the digital age, reputational damage travels fast.

Public disputes with tax authorities often make headlines. For larger companies, this can affect share prices and investor confidence. For SMEs, it can erode trust among customers and suppliers.

In Nigeria’s increasingly transparent financial ecosystem with BVN-linked accounts and interbank data systems tax defaults are not as easy to hide.

Trust is currency in business. Tax controversies weaken it.

Accumulated Debt Can Become Unmanageable

Many business owners delay tax payments hoping to “regularise later.” But tax debt rarely stays small.

Interest continues to accrue. Penalties increase. Back taxes may cover multiple assessment years.

When authorities finally enforce compliance, the accumulated liability can be overwhelming forcing restructuring, asset sales, or in extreme cases, insolvency.

Proactive engagement with tax authorities is usually far cheaper than waiting for enforcement.

Is There a Way Out?

Yes.

Tax authorities in Nigeria sometimes offer:

- Voluntary Assets and Income Declaration Schemes (VAIDS) (when active)

- Payment plans

- Negotiated settlements

The key is early engagement. Once enforcement actions begin, negotiating leverage reduces significantly.

Businesses struggling with tax compliance should consult qualified tax professionals and regularise their records before audits occur.

Conclusion

Failing to pay tax is not merely a regulatory oversight it is a strategic risk.

The consequences range from financial penalties and frozen accounts to legal prosecution and reputational damage. In a tightening regulatory environment where revenue authorities are under pressure to boost collections, enforcement is becoming more sophisticated and assertive.

For Nigerian businesses, tax compliance is no longer optional or easily deferred. It is part of corporate governance, investor readiness, and long-term sustainability.

The cost of non-compliance is almost always higher than the cost of compliance.

Smart businesses understand this early and act accordingly.

Comments