Company Income Tax in Nigeria Explained

For anyone running a registered business in Nigeria, Company Income Tax (CIT) is not just another regulatory checkbox it is one of the core fiscal obligations that shapes how businesses report profit, plan expansion, and manage compliance risk.

Yet, despite its importance, many entrepreneurs still find the rules confusing: Who exactly pays it? At what rate? How is profit calculated? What incentives exist? And what happens if you get it wrong?

This article breaks down Company Income Tax in Nigeria in clear, practical terms grounded in the law and current practice.

What Is Company Income Tax?

Company Income Tax (CIT) is a tax imposed on the profits of companies operating in Nigeria. It is governed primarily by the Companies Income Tax Act (CITA) and administered by the Federal Inland Revenue Service (FIRS).

CIT applies to:

- Limited liability companies

- Public companies

- Foreign companies operating in Nigeria

- Digital and non-resident companies earning Nigerian-sourced income

Sole proprietors and partnerships do not pay CIT. Instead, they are taxed under the Personal Income Tax Act (PITA).

Who Pays Company Income Tax?

Every incorporated company that earns profit in Nigeria is liable to CIT, except companies specifically exempted by law.

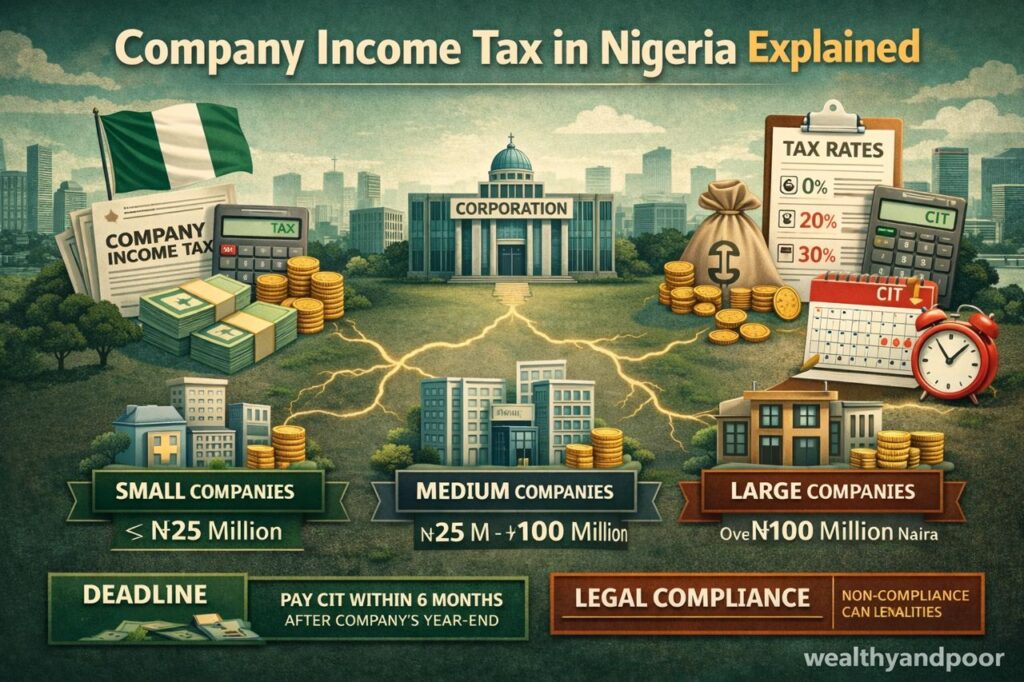

However, since the Finance Act reforms introduced in 2019 and subsequent years, Nigeria operates a tiered CIT system based on annual turnover:

- Small Companies

Annual gross turnover: ₦25 million or less

CIT rate: 0%

Small companies are exempt from paying CIT but must still file returns.

- Medium-Sized Companies

Annual turnover: Above ₦25 million but below ₦100 million

CIT rate: 20%

- Large Companies

Annual turnover: ₦100 million and above

CIT rate: 30%

This tiered structure was introduced to ease the tax burden on small businesses and encourage formalisation.

What Counts as Taxable Profit?

CIT is charged on taxable profit not total revenue.

Taxable profit is calculated as:

- Gross Income – Allowable Expenses = Taxable Profit

Gross Income Includes:

- Sales revenue

- Service income

- Investment income

- Rental income

- Other business-related earnings

Allowable Deductions Include:

- Operating expenses (rent, salaries, utilities)

- Cost of goods sold

- Depreciation (through capital allowances)

- Interest on business loans

- Pension contributions (within limits)

However, certain expenses are disallowed, such as:

- Fines and penalties

- Personal expenses

- Capital expenses not covered by capital allowance provisions

Understanding allowable and dis – allowable expenses is critical. Poor bookkeeping often leads to overpayment or worse, disputes during audits.

Filing Requirements and Deadlines

All companies including those exempt from paying CIT must file annual tax returns with FIRS.

Filing Deadline:

Within 6 months after the end of the accounting year

OR

18 months after incorporation (for new companies), whichever comes first.

Returns must include:

- Audited financial statements

- Tax computation

- Capital allowance schedule

- Evidence of tax payment (if applicable)

Failure to file attracts penalties starting at ₦25,000 for the first month and ₦5,000 for each additional month of default.

Minimum Tax: What If Your Company Makes No Profit?

One of the most misunderstood aspects of Nigerian CIT is minimum tax.

Even if a company declares little or no profit, it may still be required to pay a minimum tax calculated as a percentage of turnover.

However, small companies (turnover below ₦25 million) are exempt from minimum tax.

The minimum tax rule prevents companies from perpetually declaring losses to avoid tax liability.

Capital Allowances: Reducing Tax Legally

Unlike accounting depreciation, tax law allows companies to claim capital allowances on qualifying assets such as:

- Machinery

- Equipment

- Vehicles

- Buildings used for business

Capital allowance reduces taxable profit and therefore reduces CIT liability.

Nigeria provides:

- Initial Allowance (granted in the first year)

- Annual Allowance (spread over subsequent years)

- Proper asset documentation is essential to claim these benefits.

- Tax Incentives and Exemptions

Nigeria offers several tax incentives to encourage investment:

- Pioneer Status Incentive

Companies operating in approved industries may enjoy up to 3–5 years of tax holiday under the Nigerian Investment Promotion Commission (NIPC).

- Export Incentives

Companies involved in export processing zones may receive tax concessions.

- Rural Investment Allowance

Granted for businesses operating in underserved areas.

Businesses should evaluate whether they qualify for incentives before filing.

Withholding Tax and Company Income Tax

Withholding Tax (WHT) is often confused with CIT.

WHT is not a separate tax. It is an advance payment of income tax deducted at source from certain transactions, such as:

- Contracts

- Consultancy services

- Rent

- Dividends

WHT credits can be used to offset CIT liability at year-end.

What Happens If a Company Fails to Pay CIT?

Failure to comply can result in:

- Financial penalties and interest

- Tax audits

- Freezing of bank accounts (via court order)

- Legal proceedings

- Loss of Tax Clearance Certificate (TCC)

Without a valid TCC, companies may be unable to:

- Bid for government contracts

- Access certain loans

- Secure regulatory approvals

In recent years, enforcement has become more digital and data-driven, making non-compliance increasingly risky.

Company Income Tax and Nigeria’s Economic Reality

Nigeria’s tax-to-GDP ratio remains among the lowest globally. As a result, the government continues to expand the tax base rather than increase rates significantly.

This means:

- Greater scrutiny of corporate records

- Increased audits

- Stronger inter-agency data sharing

For businesses, compliance is no longer optional or easily delayed.

Conclusion

Company Income Tax in Nigeria is more structured today than it was a decade ago. The tiered rate system provides relief for small businesses, while enforcement mechanisms have become more sophisticated.

For business owners, the goal should not simply be “paying tax,” but understanding the system well enough to:

Avoid penalties

Claim legitimate deductions

Utilise available incentives

Maintain audit-ready financial records

In the long run, tax compliance strengthens credibility, improves investor confidence, and positions a business for sustainable growth.

Company Income Tax is not just a statutory obligation it is a core part of responsible corporate governance in Nigeria’s evolving business landscape.

Comments