How Much Company Income Tax Do SMEs Pay?

Small and Medium Enterprises (SMEs) form the backbone of Nigeria’s economy, accounting for a large share of employment, innovation, and local economic activity. Yet, taxation remains one of the most misunderstood aspects of running a small business. Many entrepreneurs assume that all companies must pay the same level of corporate tax, but Nigeria’s tax framework actually uses a tiered system designed to support small businesses.

Company Income Tax (CIT) is the primary tax that incorporated businesses pay on their profits. However, the amount SMEs pay depends largely on their annual turnover and profit levels. Understanding how the tax structure works is essential for entrepreneurs, investors, and policymakers interested in Nigeria’s SME ecosystem.

This article explains how much company income tax SMEs pay, how the rates are calculated, and what obligations still apply even when tax is zero.

What Is Company Income Tax?

Company Income Tax (CIT) is a tax imposed on the profits of companies operating in Nigeria. The tax is governed by the Companies Income Tax Act (CITA) and administered by the Federal Inland Revenue Service (FIRS).

Unlike many other taxes, CIT is not charged on a company’s revenue but on its taxable profits after deducting allowable business expenses such as salaries, rent, equipment purchases, and other operational costs.

For example, if a business earns ₦10 million in revenue but spends ₦6 million on expenses, its taxable profit becomes ₦4 million. The applicable CIT rate is then applied to that profit.

CIT Rates for SMEs in Nigeria

Nigeria introduced a tiered corporate tax system to reduce the burden on small businesses and encourage entrepreneurship. The system divides companies into categories based on annual turnover.

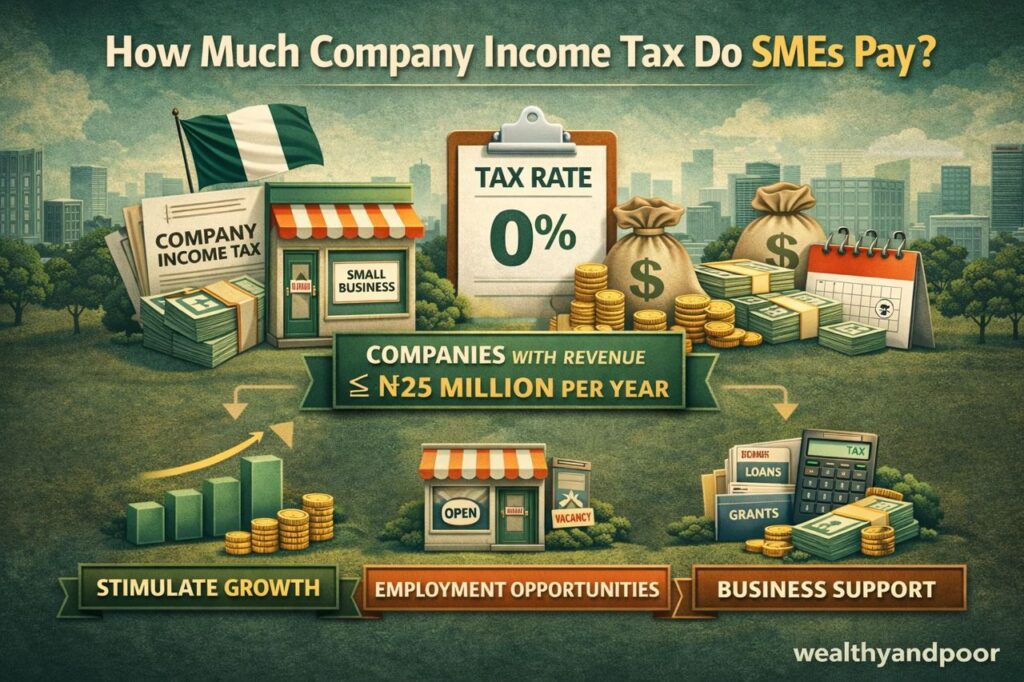

- Small Companies: 0% Company Income Tax

Small companies enjoy the most significant relief.

A company is generally classified as small if its annual turnover falls below certain thresholds. Under Nigeria’s SME tax framework, companies with low turnover are exempt from paying company income tax.

Typical thresholds used in the tax system include:

- Turnover of ₦25 million or less: 0% CIT

In some recent tax reform discussions, the exemption threshold has been extended to companies earning up to ₦100 million annually, allowing more SMEs to benefit from zero corporate tax.

This means many small businesses legally pay no company income tax at all.

The rationale behind this policy is to help startups and small enterprises reinvest their profits into growth rather than paying corporate tax too early.

- Medium-Sized Companies: 20% CIT

Businesses that grow beyond the small-company threshold move into the medium company category.

These companies typically have annual turnover between:

- ₦25 million and ₦100 million

They pay a reduced corporate tax rate of 20% on taxable profits.

This reduced rate is still lower than the standard corporate tax rate applied to larger corporations.

Example

A manufacturing SME with:

- Revenue: ₦60 million

- Expenses: ₦40 million

- Taxable profit: ₦20 million

CIT calculation:

- 20% × ₦20 million = ₦4 million tax payable

The reduced rate helps growing businesses maintain liquidity while expanding operations.

- Large Companies: 30% CIT

Once a company’s annual turnover exceeds ₦100 million, it is classified as a large company and becomes subject to the standard 30% corporate income tax rate.

At this stage, the business is considered mature enough to operate under the full corporate tax regime.

For example:

- Revenue: ₦500 million

- Expenses: ₦350 million

- Taxable profit: ₦150 million

CIT calculation:

- 30% × ₦150 million = ₦45 million tax

Additional Levies and Taxes SMEs May Pay

Although some SMEs may pay 0% CIT, they are not entirely exempt from Nigeria’s tax system. Several other obligations may still apply.

- Value Added Tax (VAT)

Businesses must charge and remit 7.5% VAT on taxable goods and services sold to customers.

However, VAT is not a cost to the business itself it is collected from customers and remitted to the government.

- Withholding Tax (WHT)

Companies are required to deduct withholding tax of about 5%–10% on certain payments such as contracts, rents, and professional services.

This tax is deducted at source and remitted to the government.

- Payroll and Employee Taxes

Employers must also handle taxes and contributions related to employees, including:

- PAYE (Pay-As-You-Earn income tax)

- Pension contributions

- Industrial Training Fund contributions

- National Housing Fund deductions

These are compliance responsibilities even if the company itself pays no CIT.

Filing Requirements for SMEs

A common misconception among entrepreneurs is that a 0% tax rate means no tax obligations. In reality, even companies exempt from paying CIT must still comply with tax filing rules.

Key filing requirements include:

- Submitting annual tax returns to the FIRS

- Keeping proper accounting records

- Filing within six months after the financial year ends

- Failure to file returns can lead to penalties and possible tax audits.

In other words, zero tax does not mean zero compliance.

Why Nigeria Introduced Tax Relief for SMEs

The Nigerian government introduced SME tax relief through reforms such as the Finance Act 2019 and subsequent tax policy adjustments to stimulate business growth.

The objectives include:

- Encouraging entrepreneurship

- Supporting small business survival

- Promoting formal business registration

- Improving long-term tax compliance

By reducing early tax burdens, policymakers hope SMEs will grow into larger companies that eventually contribute more revenue to the tax system.

Conclusion

Company Income Tax for SMEs in Nigeria depends largely on annual turnover and taxable profit.

In simple terms:

Small companies: 0% CIT

Medium companies: 20% CIT

Large companies: 30% CIT

This tiered structure allows smaller businesses to grow without immediate tax pressure while ensuring larger corporations contribute more to government revenue.

However, even SMEs that pay no company income tax must still comply with other tax obligations such as VAT, payroll deductions, and annual tax filings.

For entrepreneurs, understanding these rules is critical. Proper tax planning not only helps businesses remain compliant but also ensures they take full advantage of government incentives designed to support SME growth.

As Nigeria continues to reform its fiscal framework, SMEs that maintain accurate financial records and comply with tax regulations will be better positioned to access government contracts, funding opportunities, and long-term business growth.

Comments