Current VAT Rate in Nigeria Explained

Value Added Tax (VAT) remains one of the most important sources of non-oil revenue for the Nigerian government. As Nigeria continues to diversify away from oil dependence, consumption taxes like VAT play a growing role in funding public services and supporting government budgets.

For businesses, investors, and everyday consumers, understanding how VAT works including the current rate, what it applies to, and how it affects transactions is essential. This article explains the current VAT rate in Nigeria, how it operates, and its significance in the country’s fiscal system.

What is VAT?

Value Added Tax (VAT) is a consumption tax charged on goods and services at each stage of production or distribution where value is added. Unlike income tax, VAT is not paid directly based on earnings; instead, it is paid by consumers when purchasing taxable goods or services.

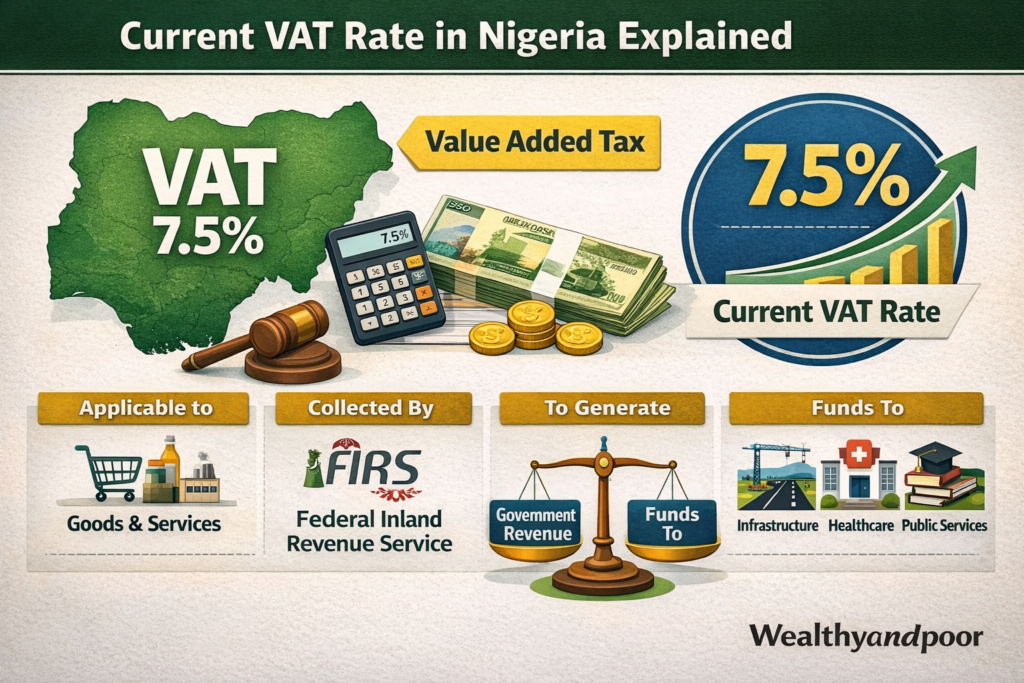

Businesses act mainly as collection agents for the government. They charge VAT on eligible goods and services, collect the tax from customers, and remit it to the government through the relevant tax authority.

The tax is administered primarily by Nigeria’s federal tax authority, the Federal Inland Revenue Service (FIRS), which is responsible for monitoring compliance and ensuring proper remittance.

Current VAT Rate in Nigeria

The current VAT rate in Nigeria is 7.5%. This rate applies to most goods and services that are not exempt under the country’s VAT laws.

Nigeria previously maintained a VAT rate of 5% for more than two decades, but this changed in February 2020, when the federal government increased the rate to 7.5% as part of fiscal reforms aimed at boosting non-oil revenue.

The adjustment was introduced through amendments to Nigeria’s tax legislation and has remained the official VAT rate in the country since then.

Why the VAT Rate Was Increased

The increase from 5% to 7.5% was part of broader efforts to strengthen government revenue and reduce dependence on oil earnings.

Nigeria has historically struggled with a narrow tax base and relatively low tax-to-GDP ratio compared with other emerging economies. Increasing VAT was viewed as one of the most effective ways to improve government revenue without significantly increasing direct taxation on income.

Analysts also note that VAT is easier to collect than many other forms of tax because it is embedded in everyday transactions.

What Goods and Services Attract VAT?

In Nigeria, VAT is generally applied to most goods and services consumed within the country, except those specifically listed as exempt or zero-rated under the VAT Act.

Examples of goods and services that typically attract VAT include:

- Professional services

- Telecommunications services

- Banking service charges

- Consultancy services

- Hospitality services

- Digital services and online platforms

For instance, banks often charge VAT on service fees such as SMS alerts, card maintenance charges, and certain transaction processing fees. These deductions may appear as small charges on customer bank statements.

The VAT is applied only to the service charge, not to the total amount in a customer’s account or transferred funds.

Expansion of VAT to the Digital Economy

Nigeria’s tax authorities have also expanded VAT coverage to include digital services and online transactions as the digital economy continues to grow.

Under new compliance frameworks, foreign and local digital service providers offering services to Nigerian users are required to register for VAT, issue VAT-inclusive invoices, and remit the tax accordingly.

These services include:

- Streaming platforms

- Cloud computing services

- Software subscriptions

- Online marketplaces

- Digital advertising platforms

This expansion reflects global trends as governments increasingly seek to tax cross-border digital transactions.

How VAT Is Calculated

VAT in Nigeria is calculated as 7.5% of the value of the taxable good or service.

For example:

If a service costs ₦10,000, the VAT will be calculated as follows:

7.5% × ₦10,000 = ₦750

Total payable amount = ₦10,750

Businesses may display VAT in two ways:

- Separate charge: VAT appears as a distinct line item on the invoice

- Inclusive pricing: VAT is already embedded in the final price

Both approaches are allowed as long as the VAT component is properly accounted for.

VAT Revenue and Government Finance

VAT has become one of the fastest-growing revenue streams for Nigeria’s government.

Recent fiscal data show that VAT allocations to the federal, state, and local governments rose to about ₦7.73 trillion in 2025, highlighting the growing importance of consumption taxes in public finance.

These revenues are distributed among the three tiers of government through the Federation Account Allocation Committee (FAAC), which shares federal revenues monthly.

The rise in VAT collections has been attributed to several factors, including:

- Improved tax compliance

- Digitalization of tax systems

- Inflation and higher consumer prices

- Expansion of VAT coverage to digital services

VAT vs Other Banking Charges

Many Nigerians confuse VAT with other deductions on bank transactions. However, VAT is distinct from other statutory charges.

For example:

Electronic Money Transfer Levy (EMTL):

Flat charge of ₦50

Applies to transfers above ₦10,000

Not calculated as a percentage

VAT, by contrast:

Is a percentage tax (7.5%)

Applied to service charges rather than transaction values

Understanding the difference helps consumers interpret bank statement deductions more accurately.

Impact of VAT on Consumers and Businesses

The VAT system affects both businesses and consumers in several ways.

For consumers:

- It slightly increases the cost of taxable goods and services.

- It is often embedded in prices, meaning many consumers pay it without noticing.

For businesses:

- They must charge VAT on eligible goods and services.

- They are responsible for keeping accurate VAT records and filing returns with tax authorities.

- Non-compliance may attract penalties.

Despite these obligations, VAT is generally considered one of the most efficient tax systems because it spreads the tax burden across the entire economy.

Conclusion

Nigeria’s current VAT rate of 7.5% remains a key pillar of the country’s tax and revenue framework. As the government continues to prioritize non-oil revenue generation, VAT is expected to play an increasingly significant role in public finance.

With the expansion of VAT to digital services, improved compliance systems, and growing consumer activity, VAT collections are likely to continue rising in the coming years.

For businesses and consumers alike, understanding how VAT works from calculation to compliance is essential for navigating Nigeria’s evolving tax landscape.

Comments