How To Calculate Withholding Tax In Nigeria

Withholding Tax (WHT) remains one of the most widely applied tax mechanisms in Nigeria’s fiscal system. For many businesses, freelancers, and even property owners, understanding how to calculate WHT is not just about compliance it is essential for proper financial planning and cash flow management.

This guide breaks down the process in a clear, practical manner, offering real-world examples and professional insight.

Understanding the Basics of Withholding Tax

Withholding Tax in Nigeria is an advance payment of income tax deducted at source from certain transactions. It is not a separate tax but a prepayment that can be credited against a taxpayer’s final tax liability.

Typically, the responsibility of deducting WHT lies with the payer (individual or company), who must remit the deducted amount to the relevant tax authority usually the Federal Inland Revenue Service (FIRS) or State Internal Revenue Service.

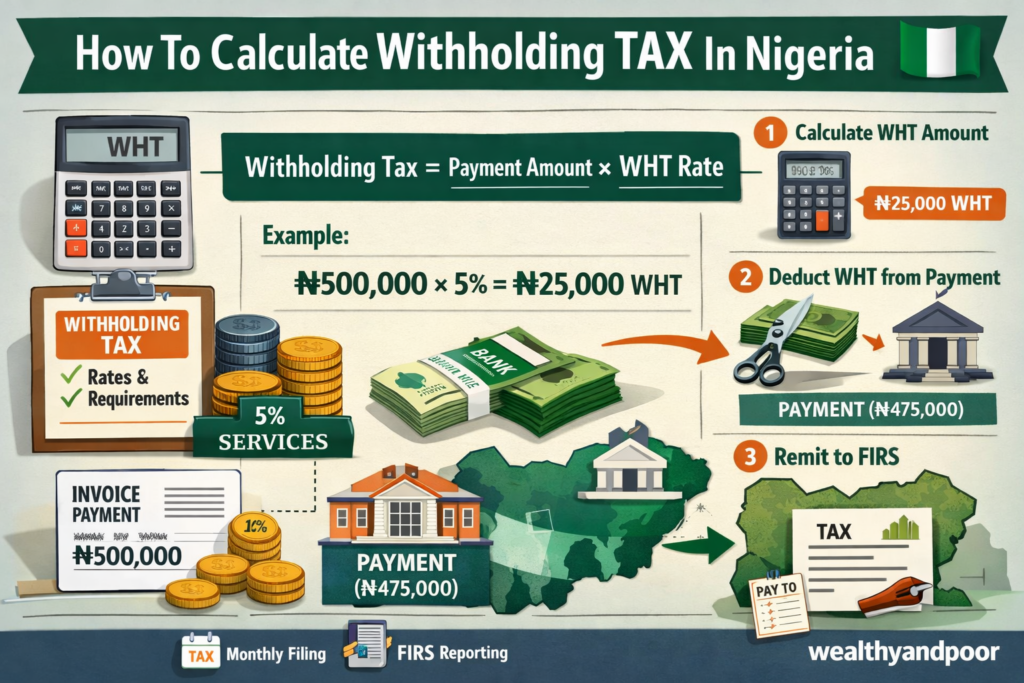

The Core Formula for Calculating WHT

At its simplest, the calculation of withholding tax follows a straightforward formula:

- Withholding Tax = Gross Payment × Applicable WHT Rate

This means that once you identify the correct rate for the transaction, calculating the tax becomes a basic multiplication exercise.

Step-by-Step Guide to Calculating WHT

- Identify the Nature of the Transaction

The first step is determining what type of payment is being made. WHT applies differently depending on the transaction, such as:

- Consultancy or professional services

- Contracts and supplies

- Rent on property

- Dividends, interest, or royalties

- Commissions or management fees

Each category attracts a specific rate under Nigerian tax regulations.

- Determine the Applicable Rate

WHT rates in Nigeria generally range between 5% and 10%, depending on the transaction type and whether the recipient is an individual or company.

Common rates include:

- 5% – Consultancy, contracts, professional services

- 10% – Rent, dividends, interest, royalties

- 2% – Supply of goods (in some cases)

For example, consultancy services provided by an individual typically attract a 5% WHT rate.

- Apply the Formula

Once the correct rate is identified, apply it to the gross transaction value.

Example 1: Consultancy Services

Contract value: ₦1,000,000

WHT rate: 5%

WHT = ₦1,000,000 × 5% = ₦50,000

Net amount paid to consultant: ₦950,000

Amount remitted to tax authority: ₦50,000

- Deduct and Remit the Tax

The payer deducts the WHT before making payment and remits it to the tax authority. The recipient is then issued a WHT credit note (certificate), which can be used to offset future tax liabilities.

- Record and Claim Tax Credit

For the recipient, WHT is not a loss of income it is a tax credit. When filing annual tax returns, the deducted amount can be used to reduce total tax payable.

Real-World Calculation Examples

Example 2: Supply of Goods

Invoice value: ₦5,000,000

WHT rate: 2%

WHT = ₦5,000,000 × 2% = ₦100,000

Supplier receives: ₦4,900,000

₦100,000 remitted as WHT

Example 3: Rent Payment

Annual rent: ₦2,400,000

WHT rate: 10%

WHT = ₦2,400,000 × 10% = ₦240,000

Landlord receives: ₦2,160,000

₦240,000 paid to tax authority

Example 4: Interest Income

Interest earned: ₦500,000

WHT rate: 10%

WHT = ₦500,000 × 10% = ₦50,000

Net interest received: ₦450,000

Key Considerations When Calculating WHT

- Gross vs Net Confusion

WHT is always calculated on the gross amount, not the net payment. Misunderstanding this is one of the most common errors in tax computation.

- Resident vs Non-Resident Rates

Non-residents may be subject to higher or flat rates (often 10%), especially for professional services and technical fees.

- Exempt Transactions

Not all transactions attract WHT. For instance, outright purchase of goods in the ordinary course of business may be exempt in certain cases.

- Timing of Remittance

WHT must typically be remitted by:

- 21st of the following month (for companies)

- 30th of the following month (for individuals)

Failure to comply attracts penalties and interest.

Common Mistakes to Avoid

- Applying the wrong rate to a transaction

- Calculating WHT on net instead of gross value

- Failing to issue WHT certificates

- Late remittance to tax authorities

- Ignoring WHT credits during annual tax filing

Why Accurate WHT Calculation Matters

Beyond compliance, proper WHT calculation helps:

- Improve financial transparency

- Avoid tax penalties

- Ensure correct tax credit utilization

- Maintain credibility with vendors and partners

For businesses, especially SMEs and startups, errors in WHT can distort financial statements and affect profitability.

Conclusion

Calculating Withholding Tax in Nigeria is relatively straightforward once the fundamentals are understood. By identifying the transaction type, applying the correct rate, and using the basic formula, taxpayers can ensure accurate deductions and full compliance with Nigerian tax laws.

However, as tax regulations evolve especially with updates from Finance Acts businesses must stay informed and, where necessary, seek professional guidance to avoid costly errors.

Comments