What Taxes Do Small Businesses Pay in Nigeria?

Running a small business in Nigeria means more than serving customers, managing staff, and watching your cash flow it also means navigating the country’s tax system. Understanding which taxes apply to your business is essential not just for compliance, but for planning, pricing and growth.

In Nigeria, taxes are collected by three levels of government: federal, state, and local. Depending on the nature of your business, its legal structure, number of employees, and annual revenue, you may pay several different taxes some mandatory and some tied to specific activities.

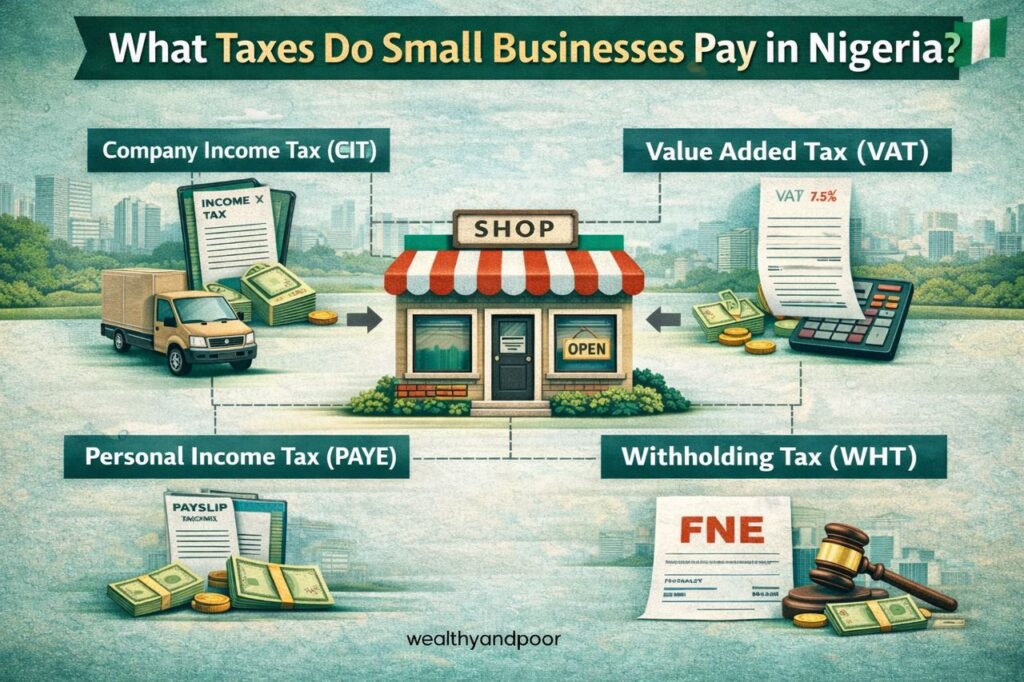

Company Income Tax (CIT) – The Federal Business Profit Tax

Company Income Tax is one of the most talked-about business taxes in Nigeria. It’s charged on net profit (not revenue) of registered companies.

What small businesses pay:

0% CIT — if your annual turnover is ₦100 million or less and your total fixed assets are ₦250 million or less. This means no corporate tax on profits, even if your business makes money.

Larger companies pay higher rates based on turnover (not directly relevant for most SMEs but good to know).

Important: being exempt doesn’t mean you stop filing returns. You still must file tax returns with the Federal Inland Revenue Service (FIRS) or the new Nigeria Revenue Service to show your business qualifies for exemption.

Personal Income Tax (PIT) and PAYE — For Sole Proprietors and Employers

If you operate a business as a sole proprietor, partnership, or LLC with employees, you’ll encounter personal income tax in two ways:

- Pay-As-You-Earn (PAYE)

PAYE is deducted from employee salaries and remitted to the State Internal Revenue Service (SIRS) on or before the 10th of each month.

Employers must calculate tax based on state tax bands and file monthly. - Personal Tax on Sole Proprietors

If you run an unincorporated business, your business income is treated as your personal income and taxed under personal income tax rules.

Note: Some states have different brackets and reliefs, but this tax is usually the responsibility of the business owner if they’re self-employed.

Value Added Tax (VAT) — A Federal Consumption Tax

Value Added Tax is another major federal tax that affects many small businesses:

Rate: 7.5% on the sale of most goods and services.

Businesses with annual turnover exceeding a threshold (often around ₦50 million) must register for VAT and charge it on their sales.

VAT is collected from customers and remitted monthly to the FIRS (or NRS).

- Even if your business isn’t required to charge VAT, you still pay VAT on goods and services you buy that are subject to VAT.Withholding Tax (WHT) — Taxis Before Payment

Withholding tax is an “advance” tax collected when payment is made for certain services or goods:

- Typical rates are 5% to 10% on payments to contractors, consultants, rent, interest and similar fees.

- Businesses must deduct WHT from payments and remit to the tax authority, issuing certificates to recipients.

These certificates can often be used as credit against their own taxes.

This is common in B2B transactions and can affect cash flows if not managed properly.

Local and State Levies — Small but Worth Tracking

In addition to federal taxes, small businesses may encounter local fees and levies, which are smaller but still mandatory:

Common levies include:

- Business Premises Levy — annual fee for operating premises.

- Advertisement and Signage Fees — if you use outdoor ads.

- Market or trade levies — set by local councils based on business activity and location.

These charges vary widely by state and local government, so it’s important to check with the authorities where your business physically operates.

Capital Gains Tax (CGT) — From Selling Assets

Capital Gains Tax applies when you sell a business asset, like land, buildings or machinery:

Typically 10% of the profit (gain) from the sale.

Note: some small businesses may be exempt or benefit from relief under specific conditions.

This is especially relevant if you’re restructuring or disposing of equipment or property.

Conclusion

Understanding your tax obligations is more than just ticking boxes it’s about keeping your business compliant, competitive, and ready for growth. Nigeria’s tax system can feel complex at first, but once you know which taxes apply to your type and size of business, it becomes easier to plan ahead, avoid penalties, and make informed financial decisions.

If your business is just starting or you’re unsure about registration and filings, consulting a qualified accountant or tax professional can be a smart investment.

Comments