Withholding Tax Rates in Nigeria Explained

Withholding Tax (WHT) remains one of the most practical tools in Nigeria’s tax system quietly deducted at source, yet central to how government tracks income and ensures compliance. For businesses, investors, and even freelancers, understanding withholding tax rates in Nigeria is not just a matter of compliance; it is essential for accurate financial planning and cash flow management.

This article breaks down the applicable rates, how they are structured, and what recent developments mean for taxpayers.

Understanding Withholding Tax in Nigeria

Withholding Tax is not a separate tax on its own; rather, it is an advance payment of income tax deducted at the point where a transaction occurs. The entity making payment whether a company, government agency, or individual deducts a percentage and remits it to the relevant tax authority.

This system ensures that tax is collected early and reduces the risk of evasion. Importantly, the amount deducted can later be used as a tax credit against the recipient’s final tax liability.

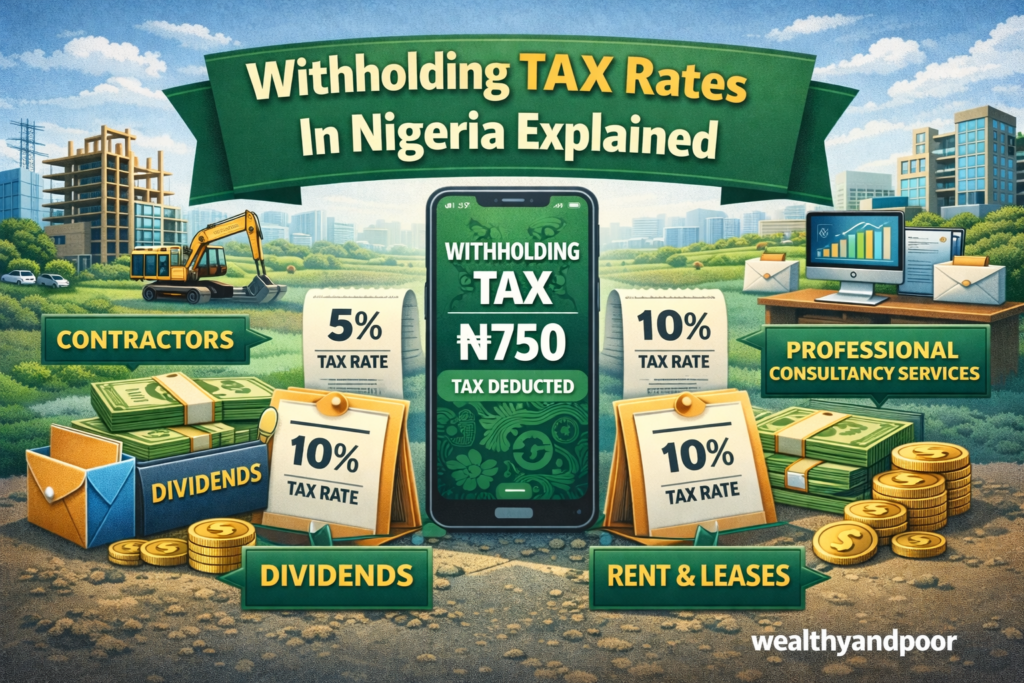

Standard Withholding Tax Rates

Nigeria’s WHT rates are largely determined by the nature of the transaction and whether the recipient is an individual, company, or non-resident.

Below is a structured breakdown of the commonly applicable rates:

- Contracts and Construction

General contracts (excluding goods): 5%

Construction and building projects: 5%

These are among the most common WHT deductions, especially in infrastructure and procurement-related transactions.

- Professional and Service-Based Payments

Consultancy services: 5% (individuals), up to 10% (companies)

Technical services: 5% – 10%

Management fees: 5% – 10%

Commissions: 5% – 10%

These rates typically apply to professionals such as consultants, contractors, and service providers.

- Passive Income (Investment-Related)

Dividends: 10%

Interest income: 10%

Rent (property or equipment): 10%

Royalties: 10% (sometimes up to 15% depending on classification)

These are often treated as final taxes in certain cases, meaning no further tax liability may arise after deduction.

- Directors’ Fees and Special Payments

Directors’ fees: 10% (can be higher under updated rules)

Specialized income streams (e.g., royalties): up to 15% in some instances

These categories are closely monitored due to their high-value nature.

- Non-Resident Transactions

Generally subject to 10% WHT across most payment types

May be treated as final tax, especially where no permanent establishment exists in Nigeria

This simplifies taxation for cross-border transactions while ensuring Nigeria captures revenue from foreign entities.

Emerging Changes in Withholding Tax Rates

Nigeria’s tax landscape is evolving, with reforms aimed at improving compliance and reducing the burden on small businesses.

Recent regulatory updates have introduced notable adjustments:

- Reduction in some service-related WHT rates (e.g., professional services reduced to around 5%)

- Lower rates (as low as 2%) for certain goods and non-specialized services

- Higher rates for specific categories, such as directors’ fees and non-resident entertainers

- Exemptions for small businesses with turnover below ₦25 million under certain conditions

These changes reflect a shift toward a more targeted and growth-friendly tax regime, especially for SMEs.

Key Principles Behind WHT Rates

Understanding the logic behind these rates helps clarify why they vary:

- Nature of Income

Passive income (like dividends or rent) generally attracts higher rates (10%), while active business transactions (like contracts) are often taxed at 5%.

- Risk of Tax Evasion

Sectors where income is harder to track such as consultancy or commissions often have higher WHT rates to ensure compliance.

- Residency Status

Non-residents are typically taxed at flat rates (around 10%), simplifying enforcement and reducing administrative complexity.

Practical Implications for Businesses

For businesses operating in Nigeria, WHT directly impacts cash flow and accounting practices.

- Cash Flow Impact: Since tax is deducted upfront, businesses receive less cash immediately.

- Tax Credits: WHT certificates must be collected and properly documented to offset final tax liabilities.

- Compliance Risks: Failure to deduct or remit WHT can attract severe penalties, including fines of up to 200% of the unpaid tax.

Common Misconceptions

- “Withholding tax is an extra tax”

This is incorrect. WHT is not an additional cost, but an advance payment of tax.

- “All transactions are subject to WHT”

Certain transactions such as outright sale of goods in the ordinary course of business may not attract WHT.

- “The rate is always 10%”

In reality, WHT rates vary significantly, ranging from 2% to 15% depending on the transaction.

Conclusion

Withholding Tax in Nigeria is both a compliance requirement and a strategic financial consideration. While the standard rates 5% for contracts and 10% for investment income form the backbone of the system, ongoing reforms are reshaping how WHT is applied across sectors.

For businesses and individuals alike, the key lies in understanding the applicable rate for each transaction, maintaining proper documentation, and leveraging WHT credits effectively.

As Nigeria continues to modernize its tax framework, staying informed about these rates is not just advisable it is essential for financial efficiency and regulatory compliance.

Comments