What Happens When Bank Systems Are Down

In Nigeria, bank system outages are a reality that affects millions of customers every year. Whether it’s an electronic funds transfer glitch, mobile app breakdown, ATM network failure, or point of sale terminal stoppage, the consequences can ripple across daily life and business.

This article explores what happens when bank systems go offline in Nigeria why it happens, how it affects people and businesses, and what banks and customers can do to cope.

What It Means for a Bank System to Be “Down”

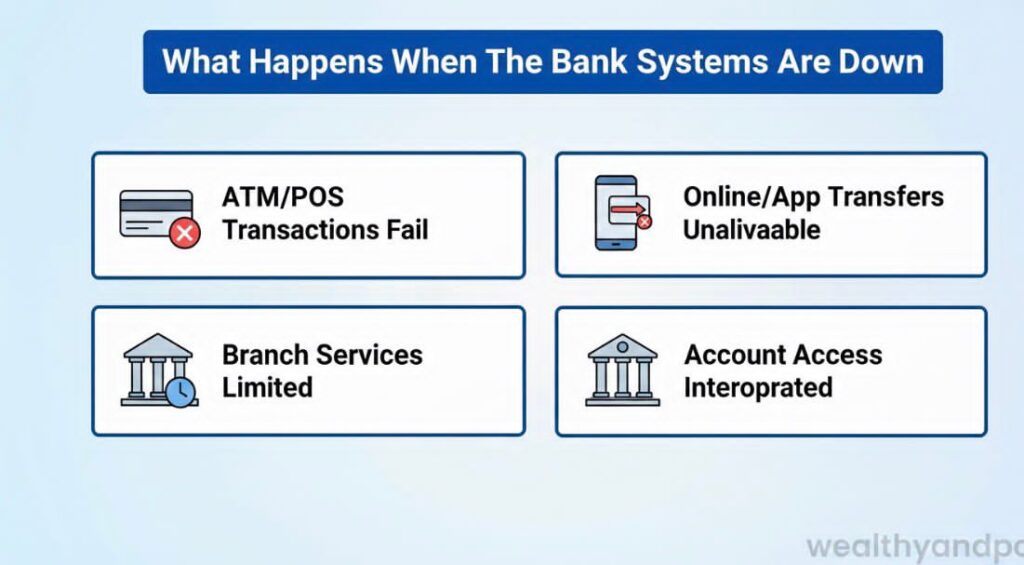

When people say a bank system is “down,” they usually mean that one or more of the bank’s electronic services are not working as expected. This can include:

- Internet and mobile banking apps

- ATM and POS (point-of-sale) transactions

- Bank transfer systems (like NIP or Interswitch)

- Card authorization platforms

- USSD codes for banking

- Internal bank tellers’ systems

A system outage doesn’t necessarily mean the bank is closed simply that the technology that supports transactions and account access isn’t functioning properly.

Common Causes of Bank System Outages in Nigeria

Banking system failures don’t happen randomly; they’re usually triggered by identifiable causes:

- Power Failures and Infrastructure Challenges : Nigeria still battles inconsistent electricity supply in many regions. When backup systems fail or are insufficient, banks can lose access to critical servers or connectivity. Power instability affects data centers and communication links, contributing to outages.

- Network or Connectivity Problems : Most banking services rely on stable internet connections and reliable telecommunications networks. When telcos experience disruptions, or fiber lines are cut (a surprisingly frequent event in Nigeria), this can hinder communication between banks and central payment systems.

- Core Banking Software Glitches : Banks use complex software platforms to manage customer accounts, process transactions, and communicate with central clearing systems. Software bugs, failed upgrades, or misconfigured updates can bring parts of these systems to a halt.

For example, a software glitch in one Nigerian bank’s system once prevented millions of customers from accessing their accounts via ATMs and mobile apps for several days forcing long queues at branches.

- Third-Party System Failures: Nigeria’s banking ecosystem depends on intermediaries such as the Nigeria Inter Bank Settlement System (NIBSS), Interswitch, and individual telecommunications providers. When any of these systems fail, the banks that rely on them feel the impact.

- Cybersecurity Threats : While rare, DDoS attacks, malware, and other cyber threats can disrupt bank systems. Banks invest heavily in defensive technologies, but the threat of attack is a constant pressure.

How System Downtime Affects Everyday People

When bank systems go down in Nigeria, the effects are often immediate and widespread. Here’s how:

- Unable to Make Transfers or Payments

One of the first impacts customers notice is the inability to send money. Whether it’s paying rent, school fees, or business suppliers, system downtime can delay transactions. Platforms like NIBSS Instant Payments (NIP) often go offline during outages, bringing transfers to a halt.

Reference example: News reports in Nigeria often cite NIBSS downtime as a key reason for failed transfers. You can see coverage of previous outages in local news archives.

- ATM and Card Transactions Fail

When switching systems like Interswitch or bank-specific authorization servers fail, customers find their ATM cards decline, even if there’s money in the account. POS terminals at shops may also fail to process payments, forcing customers to look for cash often a challenge during outages.

- Mobile and Internet Banking Stops Working

Most banks depend on internet and mobile apps for customer access. A system outage can lead to error messages like “Service Unavailable” or “Cannot Complete Your Request.” For people who rely on digital banking, this can be severely disruptive.

- Increased Foot Traffic in Branches

With electronic services down, customers often go to physical branches to request teller-assisted withdrawals or transfers. This can lead to long queues and overcrowded halls.

- Businesses Lose Sales or Delay Payments

Small businesses that rely on POS payments may lose sales if customers are unable to pay by card. Similarly, companies that depend on instant transfers for payroll or supplier payments may face operational delays.

- Customer Frustration and Loss of Trust

Repeated outages contribute to frustration among bank customers. Many complain on social media platforms like Twitter when their bank’s systems are unavailable a sign that downtime affects customer sentiment.

Real Examples of Nigerian Bank System Outages

Here are a few real-world scenarios that have made headlines:

- Central Switching System Outages

Over the years, outages on systems like Interswitch or NIBSS have caused widespread ATM and POS failures across several banks simultaneously. Such events make headlines due to their broad impact.

- Bank-Specific System Crashes

Some individual banks have experienced prolonged system failures where mobile banking, USSD services, and ATM withdrawals were unavailable for hours, even days. Customers were forced to visit branches for routine transactions.

These events are often covered in tech and business news sections of Nigerian media outlets.

How Banks and Regulators Respond to System Failures

When outages occur, banks and regulators take steps to resolve them and reassure customers:

- Technical Teams Work to Restore Service

Once an outage is reported, banks activate their IT crisis teams to identify and fix the root cause whether it’s a network issue, server crash, or software bug.

- Customer Alerts and Notices

Banks often post updates on their websites or social media accounts to notify customers about service disruptions and estimated resolution times.

- Regulatory Oversight

The Central Bank of Nigeria (CBN) and NIBSS monitor the stability of the banking infrastructure. They may engage banks and service providers to ensure systemic issues are resolved and to prevent future outages.

- Compensation and Reversals

If transactions are lost or duplicated due to system failure, banks usually correct the accounts once normal service is restored.

What Customers Can Do During a Bank System Outage

Here are practical tips for Nigerians when bank systems go down:

- Try Alternative Channels

If mobile banking isn’t working, try an ATM. If the ATM is down, try a bank branch. Sometimes only one channel is affected.

- Wait and Retry

Many outages are temporary and resolved within hours. Trying again later often works.

- Contact Customer Support

Most banks have hotlines and social media support teams that provide updates and guidance.

- Plan Ahead

If you know a major transfer or payment is needed (e.g., school fees), try to complete it earlier in the day in case an outage occurs later.

Conclusion

Bank system outages in Nigeria affect real people in real ways from failed transfers and blocked payments to long queues in branches and frustrated customers. While outages are often temporary, they reveal how heavily Nigerians rely on electronic banking for everyday life.

Understanding the causes from infrastructure challenges and software glitches to third party failures can help customers prepare and respond more effectively. And as banks continue upgrading their systems, the goal is always clear: minimize downtime and ensure smoother, more reliable banking for everyone.

Comments