Why Banks Restrict Large Transfers

In an age where money can move across borders in seconds, many bank customers are surprised or even frustrated when large transfers are delayed, queried, or outright restricted.

From sudden transfer caps to requests for additional documentation, these interruptions often feel unnecessary, especially when the funds are legitimately earned.

Yet, behind every restriction placed on a large transfer is a complex mix of regulation, risk management, and financial system protection.

Banks do not impose these limits arbitrarily. Instead, they operate within strict global and local rules designed to protect both customers and the wider economy.

This article explains why banks restrict large transfers, how these rules work in practice, and what customers should understand when moving substantial sums of money.

What Is Considered a “Large Transfer”?

There is no single global definition of a “large” transfer. What qualifies as large often depends on:

- The customer’s account history

- The country involved

- Whether the transfer is domestic or international

- Regulatory reporting thresholds

In many jurisdictions, transfers involving high value amounts (often running into thousands or millions) trigger enhanced scrutiny. Even when the money belongs entirely to the customer, the size alone can raise red flags that banks are legally required to investigate.

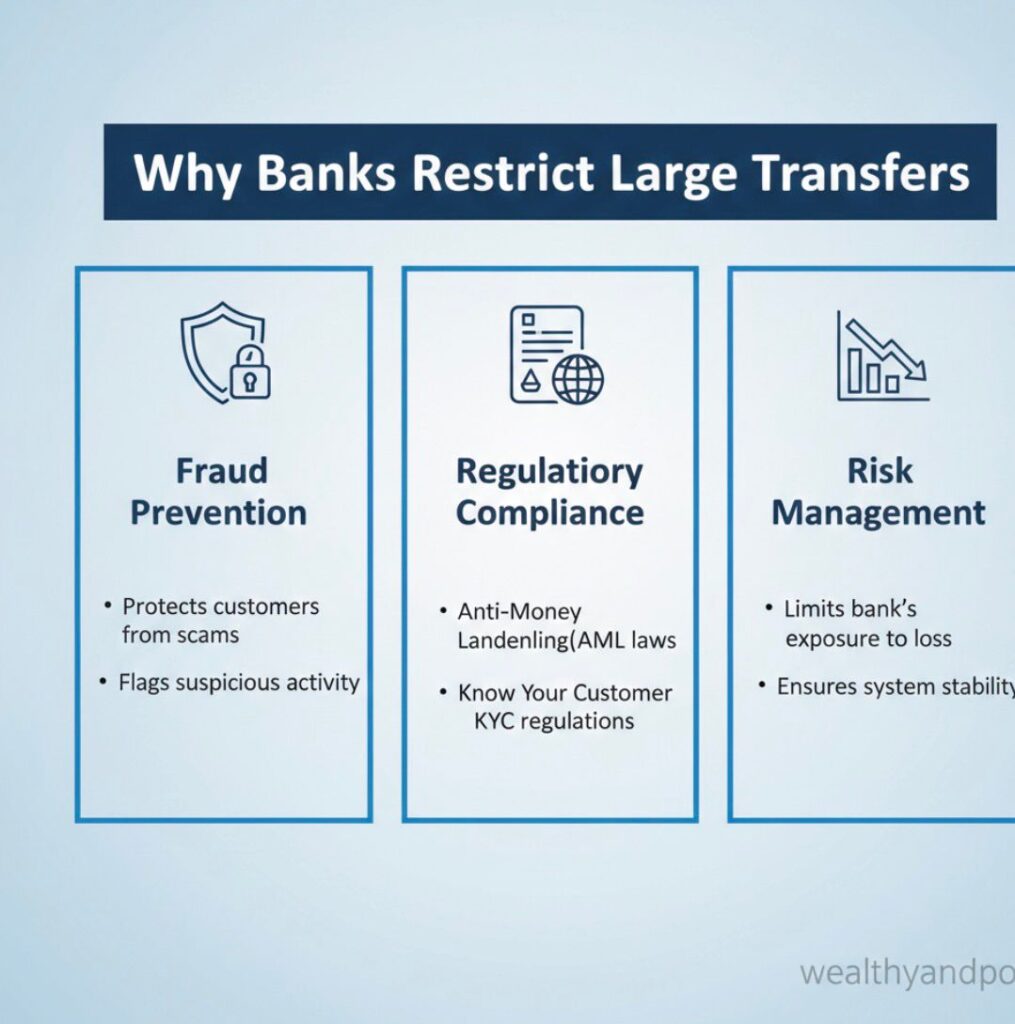

Regulatory Compliance: The Role of AML and KYC Rules

One of the strongest reasons banks restrict large transfers is regulatory compliance, especially under Anti Money Laundering (AML) and Know Your Customer (KYC) laws.

Money laundering involves disguising illegally obtained funds to make them appear legitimate. To prevent this, banks must monitor transactions, identify unusual patterns, and report suspicious activity to regulators.

For example;

In the United States, the Financial Crimes Enforcement Network (FinCEN) requires banks to monitor and report transactions that exceed certain thresholds or appear suspicious.

In the European Union, directives such as the Fifth Anti Money Laundering Directive (AMLD5) impose strict due diligence and reporting obligations on financial institutions.

By restricting or reviewing large transfers, banks ensure they are not unknowingly facilitating financial crime, terrorism financing, or tax evasion.

Risk Management and Fraud Prevention

Large transfers are prime targets for fraudsters.

A single successful fraudulent transaction involving a large amount can result in devastating losses not just for the customer, but also for the bank.

This is why banks treat high value transfers differently from everyday transactions.

Common risks include:

- Account takeovers

- Social engineering scams

- Business email compromise (BEC) fraud

- Investment and romance scams

When a transfer is unusually large or inconsistent with a customer’s normal behavior, banks may pause it to confirm that the transaction was genuinely authorized.

While this can be inconvenient, it often prevents irreversible losses.

Enhanced Monitoring and Due Diligence

When customers initiate large transfers, banks are required to conduct enhanced due diligence (EDD). This goes beyond routine checks and may involve:

- Verifying the source of funds

- Confirming the identity of the recipient

- Requesting supporting documents

- Assessing the economic purpose of the transaction

For instance, a transfer meant for overseas property purchase or major business investment may require contracts, invoices, or proof of ownership. These steps are not about mistrust they are about accountability.

Banks must be able to explain, to regulators, why a large transaction makes sense in the context of the customer’s profile.

Customer Communication and Transparency

Modern banking regulations emphasize transparency. When a large transfer exceeds preset limits, customers are usually notified and guided through the next steps.

In many cases, banks will:

- Ask customers to upgrade their account tier

- Request additional identification or documentation

- Temporarily restrict transfers until verification is completed

Clear communication helps prevent misunderstandings and reinforces trust. While the process may feel slow, it exists to protect customers from irreversible mistakes and financial exploitation.

Technology, Security, and the Future of Large Transfers

Digital banking has made transfers faster but also more vulnerable to cyber threats. To balance speed with safety, banks now rely heavily on advanced technologies.

- Artificial intelligence (AI) is used to detect abnormal transaction patterns in real time.

- Blockchain and distributed ledger technologies offer transparency and traceability for high value transfers.

- Behavioral analytics help banks distinguish genuine customers from impostors.

These tools allow banks to process legitimate large transfers more efficiently while still maintaining strong safeguards.

Final Thoughts

Banks restrict large transfers not to inconvenience customers, but to protect the financial system as a whole.

Regulatory compliance, fraud prevention, and risk management all play a role in shaping how money moves especially when the amounts involved are substantial.

Understanding these restrictions helps customers navigate banking processes with greater confidence. When large transfers are planned in advance, supported with proper documentation, and aligned with regulatory expectations, they are far more likely to proceed smoothly.

In a world where financial crime is increasingly sophisticated, cautious banking is not a weakness it is a necessity.

Comments