The Truth About Bank Loan Interest Rates in Nigeria

Bank loan interest rates in Nigeria are often described as “too high,” “exploitative,” or even “confusing.” For many borrowers whether individuals or small businesses the experience of taking a loan can feel like stepping into a financial maze. But behind the headlines and frustrations lies a more structured reality shaped by policy, risk, and economic conditions. Understanding this reality is the first step toward making smarter borrowing decisions.

What Bank Loan Interest Rates Really Mean

At its core, a loan interest rate is the cost of borrowing money. Nigerian banks typically express this in several ways: the nominal interest rate, the effective interest rate, and the Annual Percentage Rate (APR).

The nominal rate is often what banks advertise, but it does not reflect the true cost of borrowing. The effective rate includes compounding, while the APR factors in additional fees and charges giving a more accurate picture of what you will actually pay.

This distinction is crucial because many borrowers assume they are paying a lower rate than they actually are.

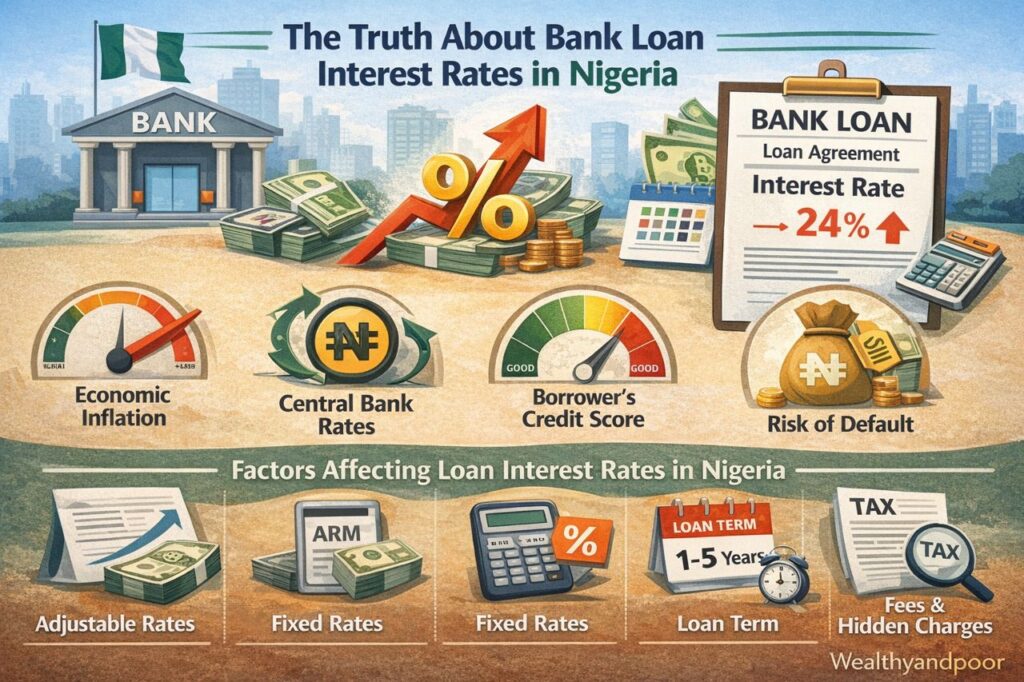

Why Interest Rates Are So High in Nigeria

One of the biggest misconceptions is that banks arbitrarily fix high interest rates. In reality, several structural factors drive lending costs in Nigeria.

- Central Bank Policy Sets the Tone

The Central Bank of Nigeria (CBN) determines the Monetary Policy Rate (MPR), which acts as a benchmark for lending across the economy. When the MPR is high as it has been in recent years (around 27%) banks naturally lend at even higher rates to remain profitable.

In simple terms:

High MPR → expensive loans

Low MPR → cheaper loans

- Inflation and Economic Instability

Nigeria’s inflation rate has remained elevated, often above 20%. When inflation is high, lenders increase interest rates to protect the real value of their money.

Banks are not just lending money they are lending future value. If inflation erodes that value, they compensate by charging more upfront.

- High Risk of Default

Nigeria has a relatively weak credit reporting culture compared to developed economies. This makes it harder for banks to assess who is likely to repay loans.

As a result, banks add a risk premium an extra cost built into interest rates to cover potential defaults.

This is why two borrowers can receive very different rates:

A “low-risk” customer gets a prime rate

A “high-risk” borrower gets a maximum lending rate

The Wide Gap Between Lending and Savings Rates

One of the most controversial aspects of Nigeria’s banking system is the large gap between what banks charge borrowers and what they pay savers.

Recent data shows:

Loan interest rates can go as high as 60%

Savings interest rates can be as low as 2.7%

This spread is often criticized as unfair. However, banks argue that operational costs, regulatory requirements, and credit risk justify the difference.

Still, for many Nigerians, the perception remains: borrowing is expensive, while saving yields little.

The Role of CBN Regulations

Another key truth is that banks do not operate in isolation. The CBN imposes strict regulations that directly affect lending rates.

For example:

High Cash Reserve Ratio (CRR) means banks must keep a large portion of deposits with the CBN, limiting funds available for lending.

Tight monetary policy reduces liquidity, making loans more expensive.

Additionally, the CBN publishes lending rates across banks to improve transparency and allow customers to compare offers.

Why Rates Vary Across Banks and Customers

Not all loan interest rates are the same. Several factors determine what you will be offered:

- Credit history: Strong repayment records attract lower rates

- Loan type: Personal loans are usually more expensive than secured loans

- Loan duration: Longer tenors often mean higher total interest

- Industry risk: Some sectors (e.g., construction or manufacturing) face higher rates due to volatility

This explains why one bank may offer 25% while another charges 40% for similar loans.

The Hidden Costs Borrowers Often Ignore

Many borrowers focus only on the interest rate and ignore additional charges that significantly increase the total cost of a loan. These include:

- Processing fees

- Insurance charges

- Management fees

- Penalties for late payment

When combined, these can push the effective borrowing cost far above the advertised rate.

Are Nigerian Bank Interest Rates Truly “Unfair”?

The answer depends on perspective.

From a borrower’s point of view, paying 30–60% interest feels excessive especially in a struggling economy.

From a banking perspective, however, these rates reflect:

- High inflation

- Regulatory constraints

- Credit risk

- Cost of funds

In essence, Nigeria’s high interest rates are less about greed and more about systemic economic challenges.

What Borrowers Should Do

Understanding the truth about interest rates is only useful if it leads to better decisions. Here are practical steps:

- Compare multiple banks before accepting a loan

- Ask for the APR, not just the nominal rate

- Negotiate where possible, especially if you have a stable income

- Consider alternative financing, such as cooperative societies or fintech lenders

Borrow only when necessary and with a clear repayment plan

Conclusion

Bank loan interest rates in Nigeria are not random, nor are they purely exploitative. They are the product of a complex financial ecosystem shaped by policy, inflation, and risk.

While the costs of borrowing remain high, informed borrowers can navigate the system more effectively. The real challenge is not just the rate itself but understanding what drives it, and how to work around it.

Comments