First bank Transfer Charges Explained

In Nigeria’s fast evolving digital banking space, understanding transfer charges is no longer optional it is essential. For customers of First Bank of Nigeria, one of the country’s oldest and most widely used financial institutions, transfer fees can vary depending on transaction type, amount, and channel used. While these charges may appear small individually, they can accumulate significantly over time, especially for individuals and businesses that transact frequently.

This article breaks down First Bank transfer charges in a clear, practical way helping you make smarter financial decisions and avoid unnecessary costs.

Understanding Transfer Charges in Nigeria

Before diving into First bank specifically, it is important to understand that Nigerian bank transfer fees are largely regulated by the Central Bank of Nigeria (CBN). Most banks including First Bank follow a structured fee model tied to transaction value bands.

These charges are typically applied when transferring money to other banks via platforms such as mobile apps, USSD, internet banking, or ATM channels.

First bank Transfer Charges Breakdown

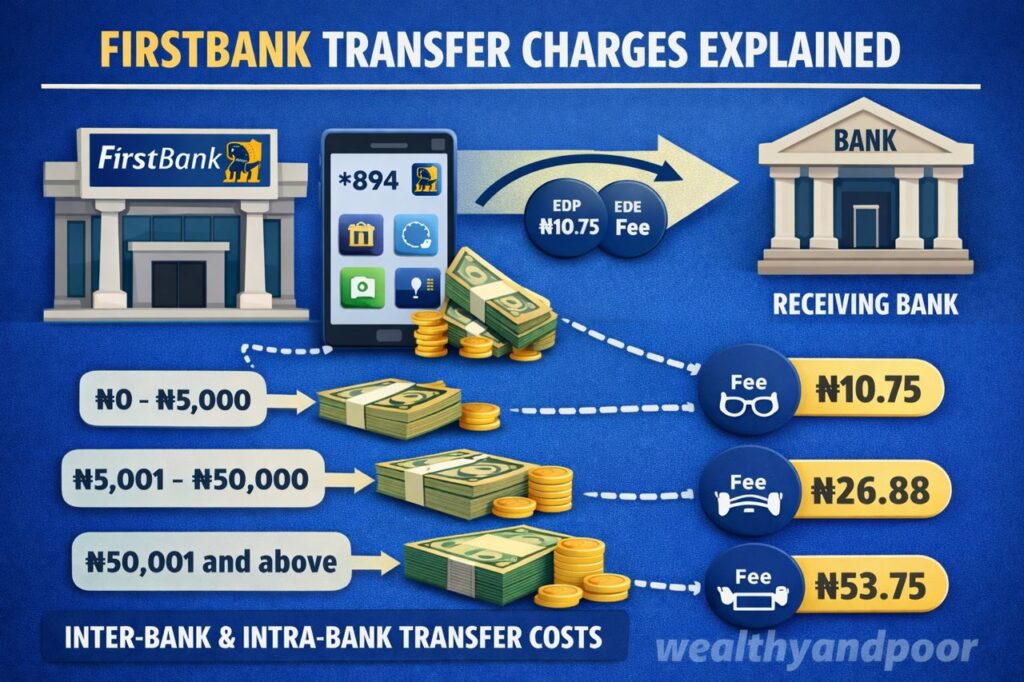

- Interbank Transfer Fees (To Other Banks)

First bank applies standard industry charges for transfers to other Nigerian banks:

- Below ₦10,000 → approximately ₦10.75

- ₦10,000 – ₦49,999 → approximately ₦26.88

- ₦50,000 and above → approximately ₦52.50

These fees are often referred to as FIP (Funds Transfer Interbank Pricing) charges, and they are consistent with CBN guidelines.

For example, if you send ₦5,000 to another bank, you pay a lower fee compared to transferring ₦100,000.

- Transfers Within First bank (Same Bank Transfers)

Transfers between First bank accounts are generally free or significantly cheaper, especially when done through digital channels like:

- First mobile app

- USSD (*894#)

- Internet banking

This is because intra bank transfers do not require interbank settlement systems, making them less costly for the bank to process.

- Stamp Duty Charges

A key charge many customers overlook is stamp duty.

- ₦50 charge on transfers of ₦10,000 and above

This is not a bank fee, but a government-imposed levy collected on behalf of the Federal Government. It applies mainly to incoming transfers or qualifying electronic transactions.

- VAT on Transfer Fees

All transfer-related fees attract Value Added Tax (VAT) of 7.5%

For instance:

- If your transfer fee is ₦50, VAT adds about ₦3.75

- Total deduction becomes slightly higher than the base fee

Though small, VAT increases the actual cost of each transaction.

- International Transfer Charges

For international transfers, First bank charges are less standardized and depend on:

- Destination country

- Currency exchange rates

- Transfer platform (e.g., remittance partners)

- Fees are typically higher than local transfers and may include:

- Processing fees

- Exchange rate margins

- Intermediary bank charges

However, in some cases, the sender (especially through remittance platforms) bears most of the cost.

- Daily Transfer Limits

Understanding limits is just as important as understanding charges:

- ₦1 million daily limit for individuals using digital banking

- Higher limits available upon request

These limits can affect how many transactions and consequently how many fees you incur daily.

Why Do These Charges Exist?

Bank transfer fees are not arbitrary. They cover:

- Payment infrastructure (e.g., NIBSS systems)

- Security and fraud prevention

- Technology maintenance

- Regulatory compliance

In essence, you are paying for the convenience of instant, secure money movement.

How to Reduce First bank Transfer Costs

Smart customers can minimize transfer expenses by adopting a few strategies:

- Batch Your Transactions

Instead of sending money multiple times, combine payments into a single transfer where possible.

- Use Same-Bank Transfers

Encourage frequent recipients (family, staff, business partners) to open First bank accounts to enjoy free transfers.

- Avoid Unnecessary Small Transfers

Frequent small transfers attract repeated charges these add up quickly.

- Leverage Digital Channels

USSD and mobile banking are often cheaper than branch-based transactions.

The Bigger Picture: Digital Banking and Cost Transparency

The Nigerian banking sector is gradually moving toward more transparency in fees. Customers now receive real-time breakdowns of charges before confirming transactions a welcome development.

Still, many users remain unaware of how much they spend on transfer fees monthly. In a tight economic climate, tracking these micro costs can make a meaningful difference.

Conclusion

First bank transfer charges are structured, predictable, and largely regulated but they are not insignificant. From interbank fees to VAT and stamp duty, each transaction carries a cost that can accumulate over time.

For individuals and businesses alike, the key lies in awareness and strategy. By understanding how these charges work and adjusting your transaction habits, you can retain more of your money while still enjoying the convenience of digital banking.

In today’s financial landscape, knowledge is not just power it is savings.

Comments