How Banks Use Customer Deposits

In modern banking, the money customers deposit into their accounts does far more than sit idle in a vault. It becomes the lifeblood of the financial system fueling loans, investments, and economic activity. While many depositors assume their funds remain untouched until withdrawn, the reality is more dynamic. Banks actively deploy customer deposits to generate returns, support businesses, and maintain liquidity across the economy.

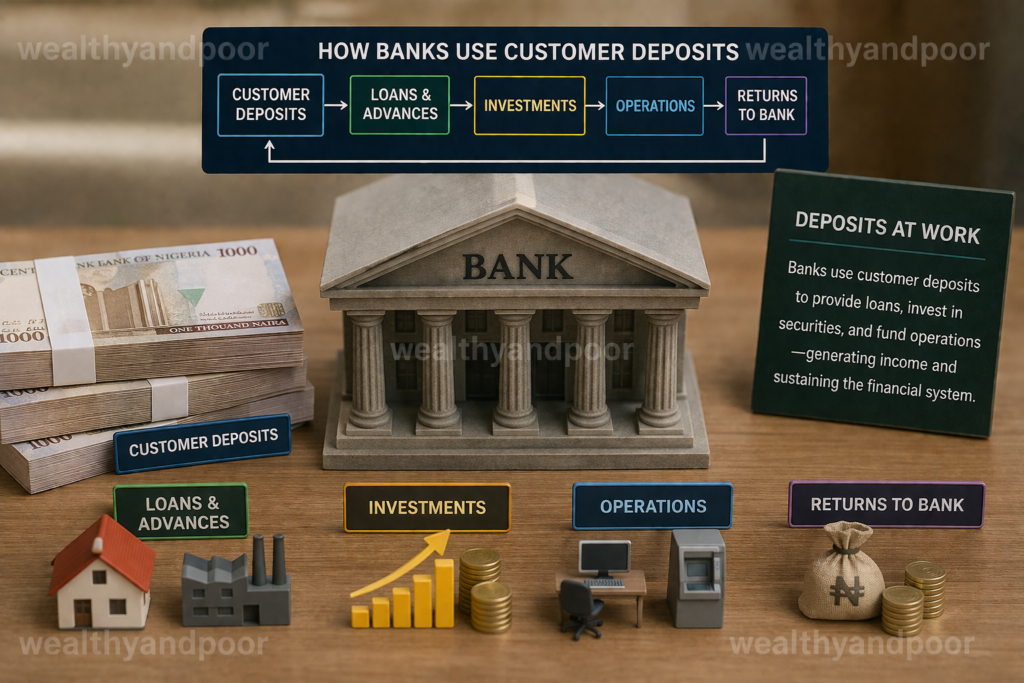

This article explores how banks use customer deposits, breaking down the process into clear structured components.

The Fundamental Principle: Deposits as Bank Liabilities

When a customer deposits money into a bank, the relationship is not one of storage but of lending. In simple terms, the depositor is effectively lending money to the bank, which records the deposit as a liability an obligation to repay on demand.

This distinction is critical. While customers retain access to their funds, the bank gains legal control over how those funds are used. This is the foundation upon which the entire banking system operates.

Financial Intermediation: Turning Deposits into Loans

Banks act as intermediaries between savers and borrowers. The most significant use of customer deposits is lending. Instead of keeping all deposited money in reserve, banks retain only a fraction and lend out the rest to individuals, businesses, and governments.

This process, known as financial intermediation, allows banks to:

- Provide personal loans (e.g., mortgages, car loans)

- Fund business expansion

- Support government borrowing through bonds

The income generated from these loans primarily through interest payments is the core source of bank profitability. Banks typically charge borrowers higher interest rates than they pay depositors, and the difference (known as the net interest margin) forms a major portion of their earnings.

Fractional Reserve Banking: The Engine Behind Lending

A key concept underlying how banks use deposits is fractional reserve banking. Under this system, banks are required (or expected, depending on jurisdiction) to hold only a portion of deposits as liquid reserves while using the rest for lending or investment.

For example, if a bank receives ₦1,000,000 in deposits, it might keep a fraction available for withdrawals and lend out the remainder. Importantly, not all customers withdraw funds simultaneously, allowing banks to operate efficiently without holding full reserves.

This system also enables the expansion of money supply. One deposit can support multiple rounds of lending as borrowed money is spent and redeposited in the banking system a phenomenon often referred to as the money multiplier effect.

Investment Activities: Beyond Traditional Lending

Banks do not rely solely on loans to generate returns. A portion of customer deposits is also invested in relatively low-risk financial instruments, such as:

- Government bonds

- Treasury bills

- Interbank lending markets

These investments provide stable, predictable income while helping banks manage liquidity and risk.

By diversifying how deposits are used, banks balance profitability with safety, ensuring they can meet withdrawal demands while still earning returns.

Liquidity Management: Keeping Cash Available

Despite actively using deposits, banks must ensure they can meet customer withdrawals at any time. This requires careful liquidity management.

Banks maintain:

- Cash reserves (physical and digital)

- Balances with central banks

- Highly liquid assets that can be quickly converted to cash

The goal is to strike a balance keeping enough funds accessible without sacrificing the opportunity to earn income from lending and investments.

A failure in liquidity management can lead to a bank run, where many customers attempt to withdraw funds simultaneously. This is why regulatory frameworks and deposit insurance systems exist to maintain trust and stability.

Maturity Transformation: Short-Term Deposits, Long-Term Loans

Another critical function of banks is maturity transformation using short term deposits (which customers can withdraw anytime) to fund long-term loans (such as mortgages or business financing).

This transformation is essential for economic growth, as it allows long-term investments to be funded by readily available savings. However, it also introduces risk, requiring banks to carefully manage timelines and cash flows.

Why Deposits Matter to the Economy

Customer deposits are not just important for banks they are central to economic development. By channeling deposits into loans and investments, banks:

- Enable businesses to expand and hire

- Support infrastructure development

- Facilitate consumer spending

- Promote financial stability

In essence, deposits serve as the foundation for credit creation, which drives economic activity on both local and global scales.

The Profit Model: How Banks Earn from Deposits

Banks generate income from deposits in several ways:

- Interest Spread – The difference between interest earned on loans and paid on deposits

- Investment Returns – Earnings from bonds and other securities

- Fees and Charges – Account maintenance, transaction fees, and services

Among these, the interest spread remains the most significant contributor to bank profitability.

Conclusion: More Than Just Storage

Customer deposits are the cornerstone of modern banking, but they are far from passive. Once deposited, money becomes part of a broader financial system circulating through loans, investments, and economic activity.

Banks operate on trust: depositors trust that their funds will be available when needed, while banks rely on that stability to put those funds to productive use. This delicate balance between accessibility and utilization is what allows the banking system to function efficiently.

Understanding how banks use deposits not only demystifies everyday banking but also highlights the critical role individuals play in sustaining the financial ecosystem.

Comments