Treasury Bills vs Fixed Deposits: Which is Better?

In an era of rising inflation and increasing financial awareness, many Nigerians are moving beyond traditional savings accounts in search of safer and more rewarding investment options. Two of the most popular low risk instruments are Treasury Bills (T-Bills) and Fixed Deposits (FDs). While both offer stability and predictable returns, they operate differently and serve different financial goals. The real question is not just which is better but which is better for you.

Understanding the Basics

- What Are Treasury Bills?

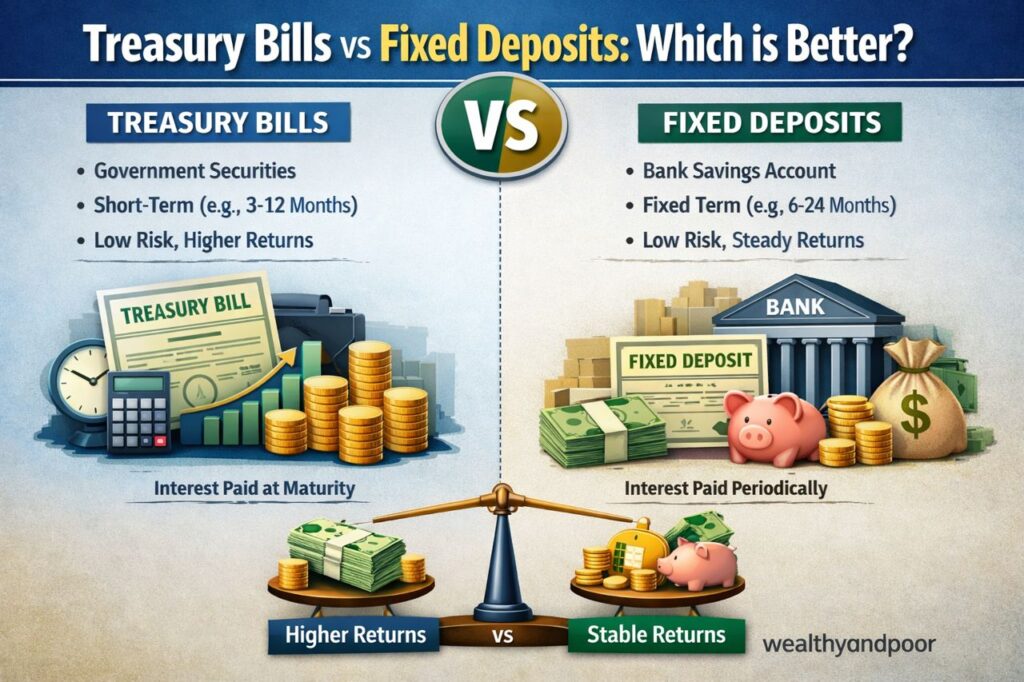

Treasury Bills are short-term debt instruments issued by the Central Bank of Nigeria on behalf of the federal government. When you invest in T-Bills, you are essentially lending money to the government for a fixed period typically 91, 182, or 364 days.

They are sold at a discount and redeemed at full value upon maturity. For instance, you might invest ₦950,000 and receive ₦1,000,000 at maturity the difference being your return.

- What Are Fixed Deposits?

Fixed Deposits are investment products offered by commercial banks. You deposit a lump sum for a predetermined period and earn a fixed interest rate. Tenures can range from 30 days to over a year, depending on your preference.

Unlike T-Bills, interest may be paid periodically or at maturity, making them attractive for those seeking steady income streams.

Key Differences Between Treasury Bills and Fixed Deposits

- Risk Profile

Both instruments are considered low risk, but there is a subtle difference. Treasury Bills are backed by the federal government, making them virtually risk-free.

Fixed Deposits, on the other hand, depend on the financial health of the bank. While banks are regulated and deposits are insured to some extent, they still carry slightly more risk than government securities.

Verdict: Treasury Bills are safer.

- Returns and Profitability

One of the most significant deciding factors is return on investment.

- Treasury Bills typically offer higher yields, often ranging from about 10% to 30% depending on market conditions.

- Fixed Deposits usually offer lower returns, often between 5% and 15%.

Additionally, T-Bill earnings are tax-free, while Fixed Deposit interest is subject to a 10% withholding tax.

Verdict: Treasury Bills generally deliver better net returns.

- Liquidity and Flexibility

Liquidity refers to how easily you can access your money.

- Treasury Bills can be sold in the secondary market before maturity, offering some flexibility.

- Fixed Deposits allow early withdrawal, but usually with penalties or reduced interest.

Verdict: Treasury Bills offer better liquidity in most cases.

- Investment Structure

The way returns are paid differs significantly:

- Treasury Bills pay interest upfront (discounted investment model).

- Fixed Deposits pay interest either periodically or at maturity.

This means T-Bills may suit investors who prefer lump-sum returns, while Fixed Deposits appeal to those who want periodic income.

- Minimum Investment Requirements

Treasury Bills can be accessed through banks or brokers, sometimes starting from around ₦50,000 in practice.

Fixed Deposits often require higher minimums depending on the bank, sometimes ₦100,000 or more.

Verdict: Both are accessible, but T-Bills can be more flexible depending on the entry route.

- Impact of Inflation

Neither investment is designed to generate massive wealth they are primarily capital preservation tools. However, inflation can erode returns.

Treasury Bills, with typically higher yields, have a better chance of beating inflation compared to Fixed Deposits.

Verdict: Treasury Bills are better positioned against inflation.

When Fixed Deposits Make More Sense

Despite the advantages of Treasury Bills, Fixed Deposits are not obsolete. They may be preferable if:

- You want predictable, regular income (monthly or quarterly interest payouts)

- You prefer a simple, bank-based investment process

- You are investing smaller amounts and negotiating better rates with banks

Fixed Deposits also offer psychological comfort for investors who prefer dealing directly with familiar banking institutions.

When Treasury Bills Are the Better Option

Treasury Bills are ideal if:

- You want higher returns with minimal risk

- You prefer tax-free earnings

- You are investing for the short term (3–12 months)

- You want better protection against inflation

They are particularly attractive in uncertain economic conditions where capital preservation and yield matter most.

The Final Verdict

So, which is better?

There is no one-size-fits-all answer but for most investors focused on maximizing returns while maintaining safety, Treasury Bills have the edge. They offer higher yields, tax advantages, and stronger security due to government backing.

However, Fixed Deposits still hold value for those who prioritize convenience, predictable income, and simplicity.

A Smarter Approach: Why Not Both?

Rather than choosing one over the other, a balanced investor may consider using both instruments:

- Allocate a portion to Treasury Bills for higher returns

- Keep some funds in Fixed Deposits for steady income and flexibility

This hybrid approach reduces risk while optimizing returns.

Conclusion

Treasury Bills and Fixed Deposits are not competitors as much as they are complementary tools in a smart investor’s portfolio. Understanding their differences risk, returns, liquidity, and taxation allows you to align your choice with your financial goals.

In today’s economic reality, letting money sit idle is no longer an option. Whether you choose Treasury Bills, Fixed Deposits, or a mix of both, the most important step is making your money work for you.

Comments