What Makes a Bank Profitable

In the world of finance, few institutions are as central and as misunderstood as banks. To the average customer, banks appear to make money simply by charging fees or lending funds. But beneath the surface lies a more complex system driven by interest spreads, operational efficiency, risk management, and diversification of income.

Understanding what truly makes a bank profitable requires looking beyond the obvious and examining the mechanics of modern banking.

- The Core Engine: Net Interest Margin (NIM)

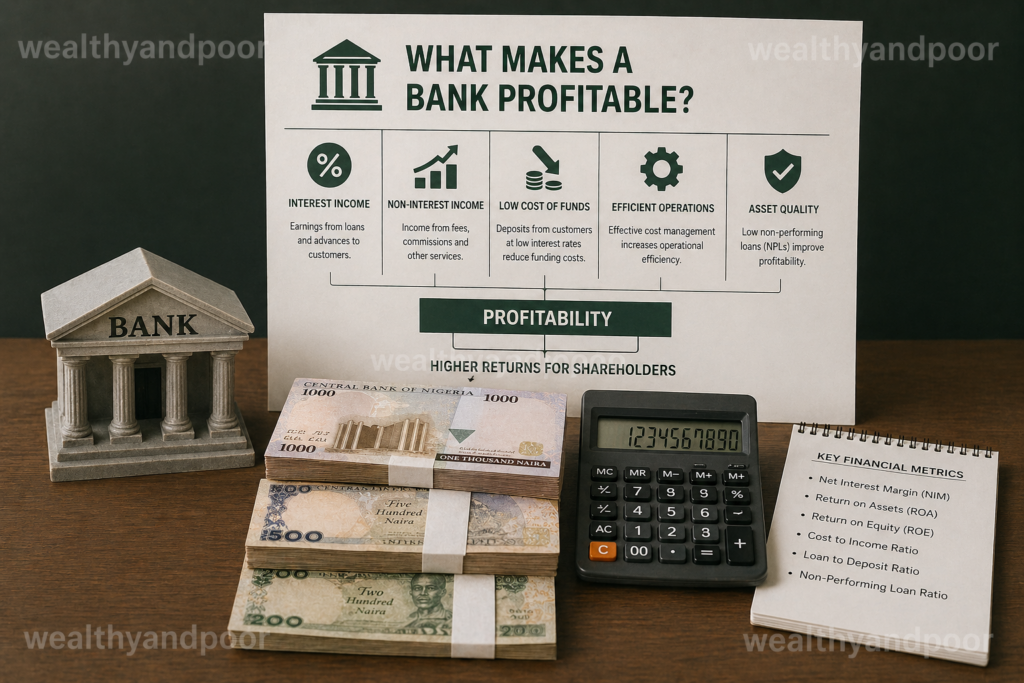

At the heart of every profitable bank lies a deceptively simple concept: earning more on loans than it pays on deposits. This difference is known as net interest income, and when expressed as a percentage of assets, it becomes the net interest margin (NIM).

Banks collect deposits from customers often paying relatively low interest and lend that money out at higher rates through loans, mortgages, and credit facilities. The spread between these rates is the primary source of income. In fact, net interest income typically accounts for 60% to 85% of a bank’s total revenue, making it the single most important profitability driver.

Even small improvements in NIM can significantly boost profits. A slight increase in lending rates or reduction in deposit costs can translate into millions in additional earnings for large institutions.

- Loan Growth and Asset Quality

Profitability is not just about margins it’s also about scale and quality. A bank that successfully grows its loan book increases its interest-earning assets, thereby expanding revenue potential.

However, not all loans are equal. High risk loans may offer higher interest rates, but they also increase the likelihood of defaults. When borrowers fail to repay, banks must make provisions for credit losses, which directly reduce profits.

Strong banks strike a balance between growth and risk management. They focus on high quality borrowers, diversify their loan portfolios, and maintain strict credit standards. Sustainable profitability depends not just on how much a bank lends, but how well those loans perform over time.

- Diversified Revenue Streams

While interest income dominates, modern banks no longer rely on it alone. A growing share of profitability comes from non-interest income, including:

- Account maintenance fees

- Transaction and card charges

- Wealth management services

- Investment banking and advisory fees

For many banks, these sources contribute 30% to 40% of total revenue, providing a buffer against fluctuations in interest rates.

This diversification is critical. When interest margins shrink such as during periods of low interest rates fee based income can stabilize earnings and protect profitability.

- Cost Efficiency and Operational Discipline

Revenue alone does not guarantee profitability. A bank must also manage its expenses effectively. Operating costs such as staff salaries, branch networks, technology systems, and regulatory compliance can significantly erode profits if not controlled.

One key metric investors watch is the cost to income ratio, which measures how efficiently a bank converts revenue into profit. Lower ratios indicate better efficiency.

Digital transformation has become a major lever here. Banks that adopt technology to automate processes, reduce physical infrastructure, and improve customer experience often achieve higher profitability through lower operating costs.

- Funding Structure and Deposit Base

A bank’s source of funding plays a crucial role in determining its profitability. Customer deposits are typically the cheapest and most stable form of funding.

Particularly valuable are non interest bearing deposits, such as current accounts. These provide banks with “free” capital that can be lent out at market rates, significantly boosting margins.

Banks with strong deposit franchises large, loyal customer bases enjoy a structural advantage over competitors that rely more heavily on expensive wholesale funding.

- Interest Rate Environment

The broader economic environment, especially interest rates, has a powerful influence on bank profitability.

Rising interest rates often expand margins, as banks can reprice loans faster than deposits.

Falling rates tend to compress margins, reducing profitability.

The shape of the yield curve also matters. A steeper curve where long term rates exceed short-term rates generally benefits banks, as they borrow short term and lend long term.

However, interest rate changes can be a double edged sword. While they may boost income, they can also affect loan demand, asset values, and borrower repayment capacity.

- Scale, Market Position, and Strategy

Larger banks often benefit from economies of scale, allowing them to spread costs across a broader asset base and invest more in technology and innovation.

At the same time, niche or specialized banks can achieve strong profitability by focusing on specific markets, such as small business lending, retail banking, or wealth management.

Ultimately, profitability is shaped by strategic choices what markets to serve, what products to offer, and how to compete.

- Risk Management and Capital Strength

Profitability without stability is short lived. Banks operate in a highly regulated environment for a reason: poor risk management can lead to catastrophic losses.

Key risks include:

- Credit risk (borrowers defaulting)

- Liquidity risk (inability to meet withdrawals)

- Market risk (losses from financial market movements)

Banks that maintain strong capital buffers and prudent risk controls are better positioned to generate consistent profits over time.

Conclusion

A profitable bank is not defined by a single factor, but by a combination of interrelated elements. At its core lies the ability to generate a healthy net interest margin. Around this foundation, successful banks build diversified income streams, manage costs efficiently, maintain strong funding bases, and navigate economic cycles with disciplined risk management.

In simple terms, banks make money by managing money carefully, strategically, and at scale. But the difference between a good bank and a great one lies in how well it balances growth, efficiency, and risk in an ever changing financial landscape.

Comments