Why Access Bank Deducts ₦50 Naira From Transfers

It’s a familiar experience for many Nigerians: after initiating a bank transfer, you notice that your account balance shows ₦50 less than expected. If you bank with Access Bank one of Nigeria’s largest commercial banks this deduction often raises questions:“Why is Access Bank removing ₦50?”, “Is this a hidden charge?”, or “Is it legal?” are common among customers who rely heavily on digital banking.

With Nigeria’s growing cashless economy and increasing dependence on mobile and online banking, understanding bank charges has become more important than ever. This article provides a clear, explanation of why Access Bank deducts ₦50 from transfers, the regulatory backing behind the charge, how it works, who it affects, and what customers can do to manage it effectively.

The ₦50 charged by Access Bank on transfers is part of a broader framework called the Electronic Money Transfer Levy (EMTL) — a flat levy applied to certain electronic transfer transactions. This charge is not unique to Access Bank; most Nigerian banks comply with it because it’s embedded in national tax regulations and Central Bank of Nigeria (CBN) guidelines.

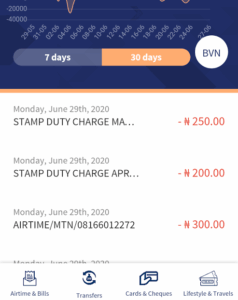

However, with the introduction of the Nigeria Tax Act, 2025, this levy has been rebranded and repositioned as a stamp duty on electronic transfers. From January 1, 2026, banks including Access Bank notified customers that a ₦50 stamp duty will be levied on electronic transfers of ₦10,000 or more, and importantly, this charge must now be borne by the sender — a shift from previous practice where the ₦50 levy was deducted from the recipient’s account, which meant beneficiaries received slightly less money than expected.

This means:

- Every transfer of ₦10,000 or more attracts ₦50 stamp duty.

- The sender pays this fee, in addition to any regular bank transfer fees.

- The fee is separate from the bank’s own transaction charges.

How the ₦50 Stamp Duty Works in Practice

Here’s what the ₦50 deduction means for you as an Access Bank customer:

- When the Charge Applies: Transfers of ₦10,000 or more: ₦50 is deducted as stamp duty. This applies whether the transfer is intrabank (between Access Bank accounts) or interbank (to other banks)

- Transfers below ₦10,000: These are exempt from the stamp duty

- Salary payments: These are typically exempt, as they’re not treated like standard transfers

- Intra-bank/Account self-transfers: Transfers between your own accounts at the same bank are generally exempt.

Illustration: If you send ₦20,000 to a friend’s account:

- Your bank deducts the amount (₦20,000).

- A stamp duty of ₦50 is deducted from your account.

If the bank also charges a service fee for the transfer (e.g., ₦25–₦50 depending on channel and amount), that fee is in addition. So, in total, you may pay slightly more than the amount you intended to send — the ₦50 isn’t a hidden penalty, but a government levy collected through your bank.

Why This Matters for Nigerian Banking Customers

While ₦50 may seem insignificant, frequent transfers can cause these charges to accumulate over time. For small business owners, freelancers, and individuals who send money regularly, understanding this fee helps in:

- Better budgeting

- Accurate financial planning

- Reducing transaction costs

- Avoiding unnecessary disputes with banks

Financial awareness is a key part of financial literacy, especially in today’s digital economy

How to Manage and Minimize the Impact

- Group large transfers instead of multiple small ones (as transfers under ₦10,000 are exempt).

- Use intra-bank transfers where possible — these are often exempt from the stamp duty.

- Understand the Access Bank rate guides

Read Also:

- Why Nigerian Banks Deduct ₦50 Naira From Transfers

- Access Bank’s Digital Innovation Honoured with Financial Inclusion Impact Award at Nexus 2025

The ₦50 deduction on Access Bank transfers is not a hidden fee or bank-imposed penalty. It is a government-mandated stamp duty applied to electronic transfers of ₦10,000 and above, collected by banks in line with Nigerian financial regulations.

As Nigeria continues to advance its cashless policy, such charges highlight the importance of transparency, financial education, and informed banking practices.

Rather than being a source of confusion, the ₦50 levy becomes easier to accept when customers understand its purpose, structure, and limits.

Comments