Account Limits For Students In Nigeria

For many young Nigerians from secondary school students to undergraduates and NYSC corps members having a bank account has become an essential part of daily life.

Whether it’s receiving allowances, paying school fees, getting paid for part time work, or simply saving money, student bank accounts are increasingly popular.

However, these accounts come with specific limits and rules that every student should understand before they open one.

This article explains why these limits exist, what typical limits look like across major banks, and what students should expect when banking in Nigeria today.

Why Student Bank Accounts Have Specific Limits

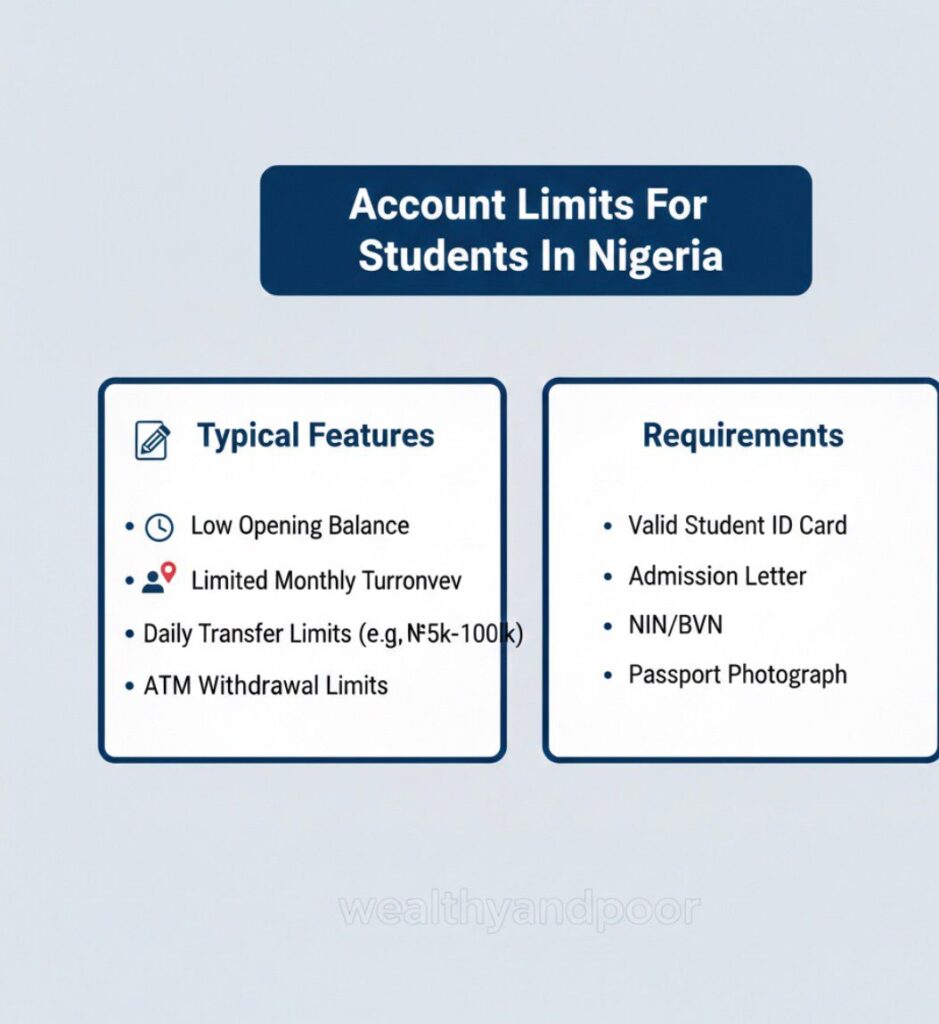

In Nigeria, banks classify accounts into different tiers based on how much documentation you provide and how the account will be used. Most student accounts fall under Tier 1 or are specially branded youth/student accounts built on this framework.

Under regulations that aim to promote financial inclusion while reducing fraud and money laundering risks, Tier 1 accounts are deliberately limited in how much money they can hold and transact.

That’s why student accounts, which often require minimal documentation, have constraints that protect both the bank and the customer.

These limitations help banks manage risk but can feel restrictive if you don’t understand them ahead of time.

What Tier 1 Limits Look Like in Practice

A typical Tier 1 account and many student accounts are set up at this level initially will have limits such as:

- Maximum cumulative account balance: ₦300,000

- Single deposit limit: Usually ₦50,000

- Daily transaction limit (including deposits, withdrawals, transfers): About ₦50,000

These limits apply to accounts opened with minimal documentation (just your National Identification Number, or NIN).

If your monthly school stipend or allowance is below these figures, a Tier 1 student account can work well.

But if you receive larger payments (say from family abroad or part time work), you may hit these ceilings quickly even if the total amount is modest in local terms.

Bank Specific Student Account Limits

Below are real examples of how Nigerian banks structure limits on student or youth accounts. These vary from one bank to another, so it’s important to check directly with the bank before you open an account.

- Zenith Bank — Aspire & Aspire Lite Accounts

Zenith Bank’s Aspire series is one of the most well known student targeted accounts:

Aspire (standard student account):

Designed for ages 16-25

Zero account opening balance

Maximum cumulative balance: ₦5,000,000

Interest-bearing savings account

Debit card available (Verve/Mastercard)

Mobile and USSD banking included

Aspire Lite (entry level):

Maximum balance: ₦300,000

Maximum single deposit: ₦50,000

Has most standard features but with lower limits

This shows how a bank can tailor student accounts for different stages with higher limits once you provide additional documentation.

- Wema Bank — Student Account

According to available guides, Wema Bank’s student account has the following limits:

Deposit limit: ₦50,000 per transaction

Maximum balance: ₦200,000

Withdrawal and transfer limits: ₦20,000 per transaction, daily max of ₦60,000

Online banking transfers: Up to ₦50,000 per transaction

These are typical of more traditional Tier 1 accounts, with modest limits that help students manage basic spending and savings.

- First Bank — Student Transfers

First Bank Nigeria doesn’t always publicly publish specific student limits, but sources suggest:

USSD transfers: Up to ₦100,000 per day

Internet/mobile banking: Can go up to ₦1,000,000 per day (depending on verification and channel)

This means a student can conduct larger transfers using digital banking platforms, once properly verified, than through basic USSD.

- Other Bank Options with Student-Friendly Features

Several other banks offer accounts targeted at young customers. While they may not explicitly state “student account limits” publicly, they typically provide products aimed at low charges, flexible access, and digital banking: - Access Bank Solo / Early Savers: Designed for students and youth, no minimum balance.

- UBA NextGen: Zero opening balance with mobile access.

- GTBank SKS / GT Creat: Options for under 18 s and undergraduates with free debit cards.

- Stanbic IBTC Blu Edge: Zero balance with debit card and savings tools.

- Sterling Trybe One: Youth account with digital incentives.

These accounts usually have higher practical limits relative to simple Tier 1 requirements, especially when linked with mobile or online banking platforms.

ATM and Withdrawal Limits

It’s also important to note that ATM withdrawal limits are often separate from your account limits, and can vary by bank and by branch.

Many banks cap how much cash you can withdraw per day sometimes lower than your account balance to manage cash distribution and security. For example, reviews across Nigerian banks show limits like N20,000–N100,000 per day at ATMs, depending on branch policies and broader regulatory cash policies.

In late 2025 and early 2026, Nigeria’s central bank introduced weekly withdrawal limits for individuals to promote cashless banking, so some banks now enforce weekly cash ceilings as well.

What Happens When You Reach Your Account Limits

If you hit your maximum allowed balance on a student or Tier 1 account, one of these usually happens:

- Incoming transfers that would push the account over the cap are rejected or returned.

- Deposits above a single deposit limit may not be accepted until you reduce the balance or upgrade the account.

- Banks may prompt you to upgrade to a higher tier account (Tier 2 or 3), which requires more documentation but offers higher or no limits.

Upgrading often requires valid ID (including BVN and NIN) and sometimes proof of address.

Practical Advice for Nigerian Students

To get the most from your student account:

- Choose the right account for your needs some banks allow higher online transfer limits if you verify more details.

- Use mobile and internet banking these often have higher transfer ceilings.

- Monitor your balance so you don’t accidentally reach your maximum and lose incoming transfers.

- Consider upgrading to a higher tier once you have full documentation if your banking needs grow.

Conclusion

Student bank accounts in Nigeria are a practical banking solution with built-in limits designed to protect young customers and the financial system.

From the ₦200,000–₦300,000 balance ceilings common in Tier 1 accounts to higher limits available via upgraded or digital banking channels, these products give students access to the formal financial system while teaching responsible money management.

Before choosing any account, it’s wise to consult directly with the bank or check their official product pages, as terms and limits change over time.

Comments