How Much Nigerian Banks Make From Charges.

The Nigerian banking sector has evolved rapidly over the past two decades, transitioning from a largely deposit driven model to a more diversified revenue system. One of the most significant yet often overlooked sources of revenue for banks in Nigeria is the array of charges and fees levied on customers. These charges range from maintenance fees on accounts to penalties on transactions and are a substantial contributor to bank profitability.

The Structure of Banking Charges in Nigeria

Nigerian banks generate revenue from charges in several categories:

- Account Maintenance Fees: Many banks impose monthly or quarterly fees for maintaining current or savings accounts. While some accounts are fee-free, premium accounts or those with added benefits can attract charges ranging from ₦200 to over ₦5,000 per month

- Transaction Fees :Transaction-based fees are one of the largest revenue streams. These include charges on cash withdrawals, transfers (especially online or interbank), ATM usage, and debit/credit card transactions. With the growth of digital banking, banks have introduced charges for faster or convenience-driven services, such as instant transfers or mobile wallet top-up.

- Penalty and Miscellaneous : Charges Banks often earn from penalties like overdraft fees, insufficient fund fees, late payment charges on loans, and foreign exchange conversion fees. These can be particularly lucrative, as customers sometimes incur them repeatedly.

- Service Charges for Value Added Services :Services such as cheque issuance, statement printing, foreign currency transactions, and advisory services attract additional fees. Some banks also monetize premium services like investment advice, wealth management, and insurance products.

How Much Do Nigerian Banks Make from Charges?

Estimating the exact revenue from charges across all Nigerian banks can be challenging due to the diversity of fee structures and the lack of centralized reporting. However, regulatory filings and annual reports provide some insight:

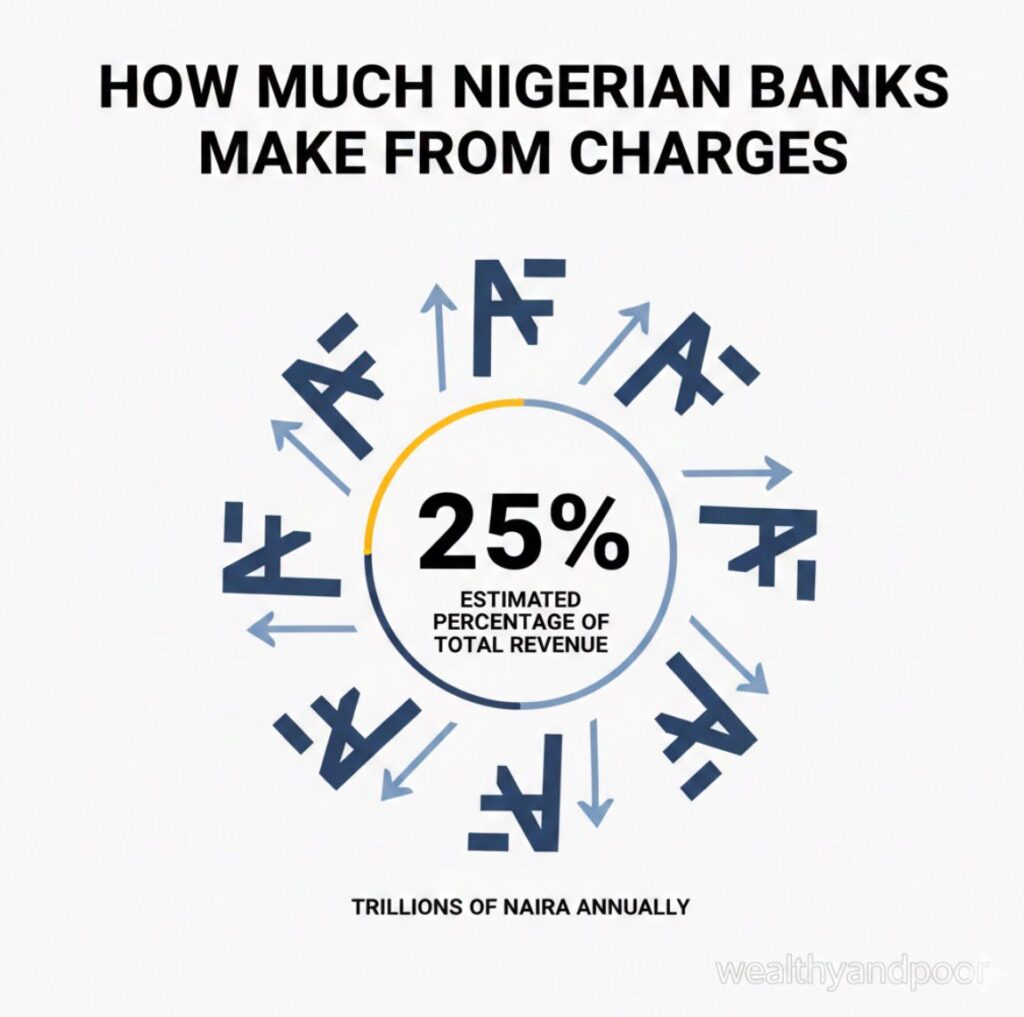

- Zenith Bank, one of Nigeria’s largest banks, reported service charges and fees constituting around 20–25% of its total non-interest income in recent years.

- Guaranty Trust Bank (GTB) has shown a similar trend, with fees and commissions making up roughly 15–20% of total operating income.

- Access Bank, after its merger with Diamond Bank, also indicated that charges on customer accounts, transfers, and trade services are significant contributors to profitability.

In 2022, estimates suggest that the top 5 Nigerian banks collectively earned over ₦200 billion annually from charges alone, reflecting both the scale of banking operations and the growing reliance on non interest income in an environment of low interest margins.

Why Charges Are Increasing.

Several factors explain why Nigerian banks are leaning heavily on fees:

- Regulatory Changes and Low Interest Margins: The Central Bank of Nigeria’s (CBN) monetary policies have kept interest rates relatively low, squeezing net interest income (NII). Banks compensate by increasing fees for services.

- Digital Transformation: With the rise of mobile banking and fintech partnerships, banks now offer instant, convenient services for which they can legitimately charge

- Operational Costs and Risk Management: Maintaining a network of branches, ATMs, and digital infrastructure is expensive. Charges help banks cover operational costs and hedge against risky transactions, such as bounced cheques or failed transfers.

The Public Debate

While banks see fees as essential revenue streams, the practice is not without controversy. Many Nigerians view excessive charges as exploitative, especially as banking fees disproportionately affect low and middle income customers. Regulators like the CBN have occasionally intervened, capping charges for certain services or promoting digital payment adoption to reduce costs for customers.

Conclusion

Charges and fees have become a cornerstone of Nigerian bank profitability, forming a significant portion of non-interest income. While they help banks manage costs, expand digital services, and maintain profitability in a low-interest environment, there is growing pressure for transparency and fairness. The challenge moving forward will be balancing profitability with customer satisfaction, ensuring that charges do not undermine financial inclusion.

In short, Nigerian banks make billions of naira annually from charges, and this revenue stream is only likely to grow as digital banking expands and new services attract fees. Understanding this dynamic is crucial for policymakers, investors, and consumers who navigate Nigeria’s financial ecosystem.

Comments