Interbank Transfer Process in Nigeria Explained

In today’s fast-paced financial ecosystem, sending money between banks in Nigeria has become almost instantaneous. Whether paying for goods, settling bills, or transferring funds to family, millions of Nigerians rely daily on interbank transfers. Yet behind the simple “transfer successful” notification lies a sophisticated system powered by advanced payment infrastructure, regulatory oversight, and real-time communication between financial institutions.

This article breaks down the interbank transfer process in Nigeria how it works, the key players involved, why delays happen, and what users should know.

What Is an Interbank Transfer?

An interbank transfer refers to the movement of funds from an account in one bank to an account in another bank. Unlike intra bank transfers (within the same bank), interbank transactions require coordination between multiple institutions and a central switching system.

For example, sending money from Access Bank to First Bank qualifies as an interbank transfer.

The Backbone of Interbank Transfers in Nigeria

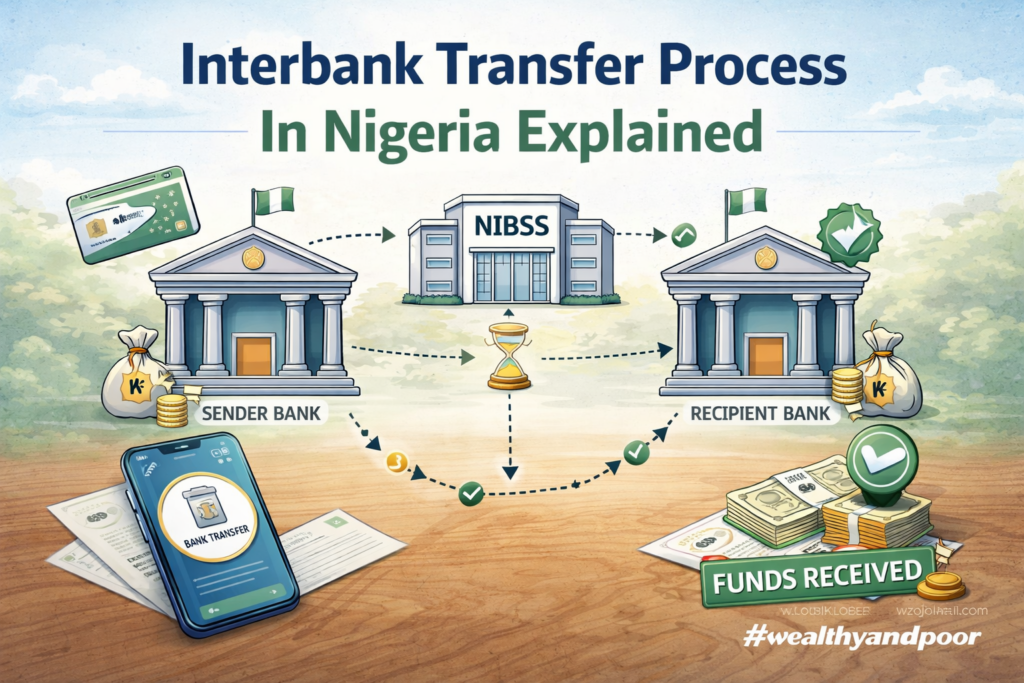

Nigeria’s interbank transfer system is largely powered by the Nigeria Inter-Bank Settlement System (NIBSS), a central infrastructure owned by the Central Bank of Nigeria (CBN) and commercial banks. NIBSS provides the platform that connects all banks and enables seamless fund transfers.

At the core of this infrastructure is the NIBSS Instant Payment (NIP) system a real-time payment solution that allows transfers to be completed within seconds, 24/7.

This system has transformed Nigeria into one of Africa’s leading digital payment markets, processing billions of transactions annually.

Step-by-Step: How Interbank Transfers Work

Understanding the process helps demystify what happens when you send money from your bank account.

- Transfer Initiation

The process begins when a customer initiates a transfer through a mobile app, USSD code, ATM, or internet banking platform. At this stage, the sender inputs details such as:

- Recipient’s account number

- Bank name

- Transfer amount

Authentication and Validation

The sending bank verifies the transaction by:

- Confirming the user’s identity (PIN, password, or OTP)

- Checking if sufficient funds are available

- Validating the recipient’s account details

If any of these checks fail, the transaction is declined immediately.

- Transmission to NIBSS (Central Switch)

Once validated, the sending bank forwards the transaction request to NIBSS through the NIP platform. This central switch acts as a clearinghouse, routing the payment instruction to the recipient’s bank.

- Processing by the Receiving Bank

The receiving bank receives the request and performs its own checks:

- Confirms the account exists

- Ensures there are no restrictions (e.g., frozen account)

If everything is in order, the bank credits the beneficiary’s account.

- Confirmation and Notification

After successful processing:

- The receiving bank sends confirmation back through NIBSS

- The sending bank notifies the sender

- The recipient receives a credit alert

This entire cycle typically takes a few seconds under normal conditions.

Clearing vs Settlement: What’s the Difference?

Two critical concepts underpin interbank transfers:

- Clearing: The process of transmitting, verifying, and reconciling payment instructions between banks.

- Settlement: The actual movement of funds between banks’ accounts, often handled later in batches through the central system.

In modern systems like NIP, clearing happens instantly, while settlement is completed shortly after in the background.

How Long Do Interbank Transfers Take?

In most cases, interbank transfers in Nigeria are completed within seconds due to the NIP infrastructure. However, timing can vary depending on system conditions and transaction type.

Older systems like NEFT could take up to 24 hours, but these are now largely replaced by real-time platforms.

Common Reasons for Delays or Failed Transfers

Despite advanced infrastructure, issues can still occur. Common causes include:

- Incorrect account details

- Network or server downtime

- Receiving bank system failures

- Transaction limits or insufficient funds

- Regulatory or fraud checks

In some cases, the system may not immediately confirm success or failure. When this happens, banks may attempt automatic reversal within a few hours.

What Happens When a Transfer Fails?

If a transfer fails:

- The funds are typically reversed to the sender’s account

- Reversals may be instant or take several hours

In rare cases, manual intervention may be required

Customers are advised to keep transaction receipts and report issues promptly to their bank.

Evolution of Interbank Transfers in Nigeria

Nigeria’s payment system has evolved significantly:

- Pre-2000s: Transfers took days and required manual processing

- NEFT era: Reduced timelines to about 24 hours

- NIP era (2011–present): Enabled instant transfers within seconds

Today, Nigeria processes billions of transactions annually, reflecting widespread adoption of digital banking.

Why Interbank Transfers Matter

Interbank transfers are central to Nigeria’s cashless economy. They enable:

- Seamless personal and business transactions

- E-commerce and digital payments

- Financial inclusion across urban and rural areas

Without this system, modern banking convenience would not be possible.

Conclusion

The interbank transfer process in Nigeria is a blend of speed, technology, and coordination. While it appears simple from a user’s perspective, it relies on a complex network involving banks, NIBSS, and real-time payment systems like NIP.

As digital banking continues to grow, improvements in infrastructure, security, and user experience will further enhance the reliability of interbank transfers. For users, understanding how the system works not only builds confidence but also helps in troubleshooting issues when they arise.

Comments