What Banks Don’t Tell You About Failed Transfers in Nigeria

In Nigeria today, millions of people rely on bank apps, USSD codes, and digital platforms to send money instantly. But when a transfer fails especially when your account is debited and the recipient never receives the funds it’s often confusing, stressful, and sometimes costly.

Many banks don’t fully explain why these failures happen or what’s really going on behind the scenes. This article digs into the common hidden factors behind failed transfers, what banks usually don’t tell customers, and how you can protect yourself.

Banks Often Don’t Explain the Complex Tech Behind Transfers

Most Nigerians assume transfers are “instant” and simple and often they are but every transfer travels through multiple systems before it’s completed.

For example: when you send money out of your bank account to another bank, that payment must be processed through the Nigeria Inter Bank Settlement System (NIBSS), which moves funds between banks’ cores.

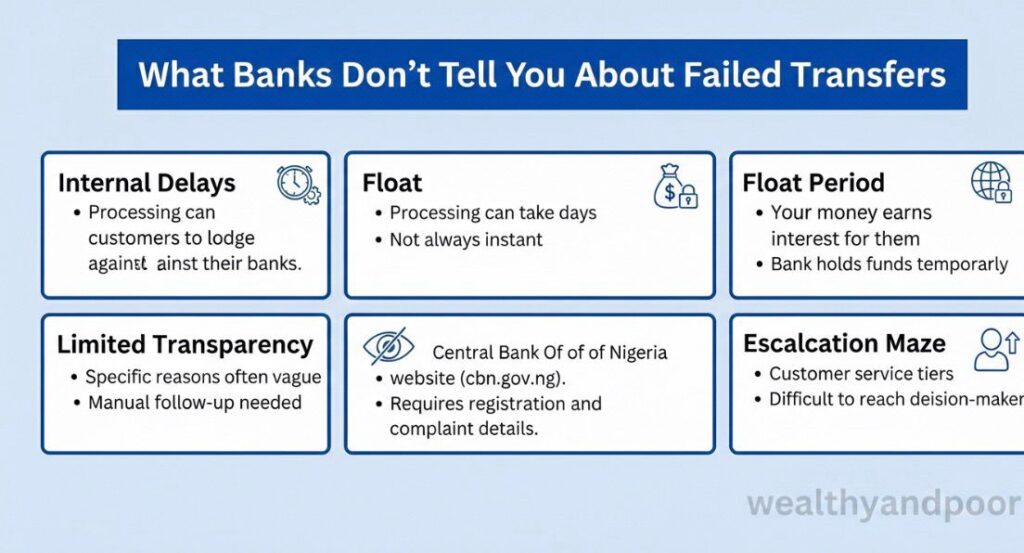

If any part of this pipeline (your bank’s servers, NIBSS infrastructure, the recipient bank’s system) is slow, offline, or congested, the transfer can fail or stay stuck. This complexity is rarely explained in customer error messages.

For example, core banking systems (the back end engines that process all transactions) sometimes have scheduled maintenance late at night or over weekends. During such maintenance, transfers might fail or be marked as pending until systems come back online even if the debit happened immediately.

Network Issues and USSD Failures Are More Common Than You Think

You’ve probably seen a message like “USSD request failed” or “Network error” but few people understand what it really means. Banks often don’t tell customers that these aren’t just random glitches, they’re tied to:

- Mobile network interruptions as you enter PINs (common in USSD transfers).

- Session timeouts if you take too long to respond on mobile menus.

- Poor integration between banks and telecom providers.

In these cases, your account might be debited and the transaction doesn’t complete because the session simply expired in the middle of processing.

Banks rarely tell you whether the failure was due to technical infrastructure, mobile network problems, or timing out routines.

Interbank Transfers Can Be Hit or Miss

Internal transfers (bank to same bank) are often faster and more reliable. But interbank transfers from Bank A to Bank B depend on coordination across multiple systems and settlement processes.

If the receiving bank’s server isn’t responding, funds can fail to credit even though your own bank shows the debit. Banks often don’t communicate this complexity; they simply say “Transaction failed.”

This is especially common during peak transaction periods like salary days, public holidays, or month end when systems are under heavy load. Many banks also schedule upgrades during weekends, which can delay settlement until Monday.

Legacy Systems Can Struggle With Today’s Volumes

Despite the surge in digital banking activity in Nigeria, many bank systems were built years ago and weren’t designed for millions of real time transactions per day. Reports show that banks still operate on older infrastructure that doesn’t scale well, leading to more failures than in many fintech services.

For example, a major analysis of failed transaction complaints in 2024–2025 showed that traditional banks like GTBank, UBA, and Zenith Bank had large numbers of customer complaints about failed transfers, slow reversals, and poor communication after system updates or outages while some fintech platforms were praised for more reliable service.

Because banks don’t want to expose internal infrastructure issues publicly, they often give generic error messages rather than detailed reasons.

Failed Transfers Don’t Always Trigger Immediate Reversals

Even when a transfer technically “fails,” banks don’t always reverse the charge instantly sometimes they wait for internal reconciliation. Banks rarely tell customers that the missing reversal isn’t the same thing as lost money:

- Failed same bank transactions are often reversed faster (sometimes within 24 hours).

- Failed interbank transactions can take longer sometimes a few days because the receiving bank needs to confirm non-credit.

This reality frustrates many customers. There’s a widespread misconception that if a transfer fails, the money should return immediately similar to how fintech wallets work but most banks still rely on batch reconciliation and manual processes.

Banks Are Limited by Central Infrastructure They Don’t Control

Whether it’s NIBSS or third party switching services, banks are part of a shared payment ecosystem. If the central switch experiences downtime, multiple banks can be affected simultaneously even if only one bank’s interface shows an error.

Many customers don’t realise that a failed transfer isn’t necessarily the bank’s fault alone. Sometimes, the issue originates in the shared payment backbone that banks simply plug into.

Regulations Exist but Customers Often Don’t Know Them

Some Nigerian banking regulations actually mandate timely reversal of failed transfers, but there’s no rule that money automatically goes to customers as compensation. For example, the Central Bank of Nigeria (CBN) set guidelines that failed inter-bank transfers (like NIBSS Instant Payments) should be reversed quickly, and banks may face fines if they delay reversal beyond specified windows but these fines are not paid to the customer directly.

Many customers believe that they should receive compensation for failed transactions but that’s not how the rules work. The fines collected by regulators are not handed to bank customers.

Banks Often Don’t Communicate Timelines Clearly

One of the biggest frustrations people report is the lack of transparency around reversal timelines. While banks may mention that they’re “investigating,” they often avoid giving firm deadlines even though regulatory guidelines set expectations.

Without clear communication, customers often don’t know when exactly their money will return or why the process is delayed and banks rarely volunteer this information unless pressed.

Fintech Alternatives Are Becoming More Transparent

One reason many Nigerians prefer fintech platforms like OPay, Moniepoint, or Palm pay is because they often provide clearer real time status updates and automatic reversals when a transfer doesn’t complete something banks lag on.

Some apps even alert you to “network or stability issues” before you confirm a transfer giving you an extra layer of confidence that the customer service channels in traditional banks don’t provide.

Your Best Defences When Transfers Fail

Since many banks don’t explain all this up front, here’s what you can do to protect yourself:

- Always save transaction receipts (screenshots, reference numbers).

- Check whether the transfer actually debited your account before retrying.

- Wait at least the regulatory reversal windows (24–72 hours for most transactions).

- Report immediately to your bank with details (date, amount, account, reference).

- Escalate to the CBN Consumer Protection Desk if the reversal takes too long.

- Consider using fintech services for frequent small transfers, since they may handle failures better.

Some of these points are backed by consumer advice from legal and banking experts, and reflect common practices around reporting and escalating failed transfers.

Conclusion

Failed bank transfers in Nigeria aren’t just one off glitches they’re often the result of complex back-end systems, shared infrastructure, legacy technology, and slow reconciliation processes that banks rarely explain to customers. While banks may provide generic error messages, the real causes often lie deeper in settlement systems, system maintenance schedules, and network dependencies.

Understanding these hidden realities and your rights as a customer can help you respond more confidently next time a transfer doesn’t go through as expected.

Comments