Why Your Bank Transfer Limit Is Low

Every day, many bank customers are surprised when they try to send money and their bank “blocks” the transaction or says they’ve hit their daily transfer limit.

This is common, especially in digital banking, mobile banking, and USSD (short code) banking platforms. But there are very real reasons behind it and most of them are designed to protect you and the financial system.

Below, we explore the main causes, what they mean, and how limits are set.

Regulatory Safety Rules (CBN Limits)

In Nigeria, a major reason transfer limits exist is because of guidelines from the Central Bank of Nigeria (CBN).

For example, the CBN once issued a daily mobile transfer limit of ₦100,000 for mobile money or USSD banking channels due to concerns about technological vulnerabilities and fraud risk.

This wasn’t arbitrary it was a directive aimed at reducing exposure to unauthorized electronic transfers.

Similarly, the CBN’s updated agent banking rules set limits on daily transactions (for example, ₦100,000 for individual customers in some contexts) to curb misuse and protect customers.

These policy limits directly affect how high your transfer limit can be on different platforms.

Security: Fraud and Hack Prevention

One of the most critical reasons banks keep low transfer limits is fraud prevention.

Banks observe thousands of suspicious activities every day stolen phones, compromised passwords, and social engineering scams all target digital transfers.

By limiting how much can be sent per day, banks reduce the potential loss if someone unauthorized gains access to your account.

Security layers like two factor authentication (2 FA), passwords, or biometric checks help, but limits still act as a second line of defense against fraud.

This is also why some fintech apps, like OPay, have features where large transfers require facial or biometric authentication before the transaction can proceed adding security and reducing fraud risk.

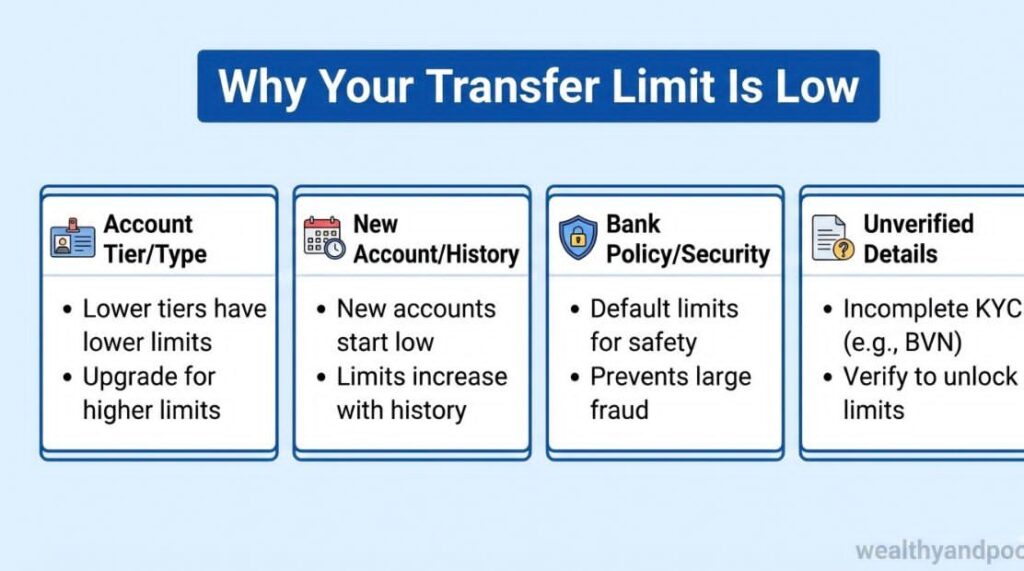

Account Verification and Know-Your-Customer (KYC)

Your transfer limit is directly tied to how much identity documentation your bank has verified.

Most banks start new accounts with basic info your name, phone number, and maybe your BVN (Bank Verification Number). But until you complete full KYC (for example, linking your National Identification Number or providing proof of address), your account is considered higher risk. Banks respond by imposing lower transfer limits.

This is particularly common if you’re using USSD (short code banking), which is easier to access but considered less secure than mobile app or internet banking. Accounts with minimal KYC (sometimes called Tier 1 accounts in Nigeria) have much lower limits than fully verified ones.

For example, someone without complete KYC might have a daily limit in the tens of thousands of naira, while a fully verified account could have a much higher limit through the bank’s mobile app.

Technology Channel Used Affects Limits

Different ways of accessing your account come with different built in rules:

- USSD (901#, 737#, etc.): Lower limits because the technology is less secure and more prone to interception.

- Mobile banking apps: Higher limits are allowed because apps use encryption and secure logins.

- Internet banking/web banking: Often the highest limits because of strong authentication and security processes.

So even with the same account, accessing it via USSD might give you a low transfer ceiling while the mobile app offers more room.

Bank Specific Risk Controls

Each bank has its internal risk assessment systems. If your transaction behavior suddenly changes (for example, sending unusually large amounts or to new beneficiaries), the bank’s system might temporarily reduce your daily limit or block the transaction until additional verification is completed. This is part of automated fraud prevention and monitoring systems.

The bank’s fraud detection sometimes powered by analytics and real time monitoring is designed to catch unusual patterns before money leaves the system. While this can be frustrating, it protects both the customer and the bank’s infrastructure.

Protection of the Financial System

Banks don’t just protect individual customers they must also safeguard the entire financial system.

Massive transfers across many accounts at once could destabilize the payment networks if something goes wrong. Low limits help keep transaction flows controlled and manageable, particularly during peak times or when technical issues occur.

This is part of why regulators like the CBN keep limits in place: they help reduce systemic risk.

Customer Trust and Operational Risk

When a bank processes millions of transfers daily, it has to ensure it can handle errors, reversals, and customer disputes.

For example, if someone sends funds to the wrong account by mistake a common situation banks often have complicated processes to resolve it. Knowing that small mistakes are easier to reverse than large ones is one reason daily limits exist.

By keeping transfer limits at reasonable thresholds, banks reduce errors and operational risk, leading to more stable services for all customers.

How to Raise Your Transfer Limit

If you feel your transfer limit is too low, here are common ways to increase it:

- Complete full KYC: Provide all required identification documents so your bank can verify your profile.

- Use secure channels: Access your account via the bank’s official mobile app or online banking instead of just USSD.

- Request limit increase: Some banks allow you to submit a request (sometimes in-app or at a branch) to raise your daily limit.

- Link BVN and NIN: In Nigeria, linking your BVN and NIN often unlocks higher transfer limits.

These steps often unlock higher limits because they indicate to the bank that you are a verified, low risk customer.

Summary

In simple terms, your transfer limit is likely low because of a combination of Regulatory directives aimed at reducing fraud and protecting the banking system also Security risk controls that protect your money from unauthorized access or Incomplete account verification (KYC).

Different technologies (USSD vs. app vs. internet banking) have different limits.

Hence, Bank level risk monitoring systems that automatically adjust limits.

Low limits may feel inconvenient, but they are part of how banks protect you and the banking system from fraud, errors, and risk.

Comments