Tier 1 vs Tier 2 vs Tier 3 Account Comparison

In modern banking and financial systems, accounts are often classified into “tiers.” These tiers aren’t about quality or prestige , they’re about documentation, verification, and the features or limits a customer can access.

This system helps banks balance financial inclusion with regulatory compliance and fraud prevention.

What Are Account Tiers?

Account tiers are levels assigned to bank accounts based on how much personal information the customer has provided and verified. Each tier comes with different limits on transactions, balance caps, and access to banking features.

In many countries including Nigeria banks follow guidelines (often set by regulators like the Central Bank) that define what’s required for each tier and what privileges it carries.

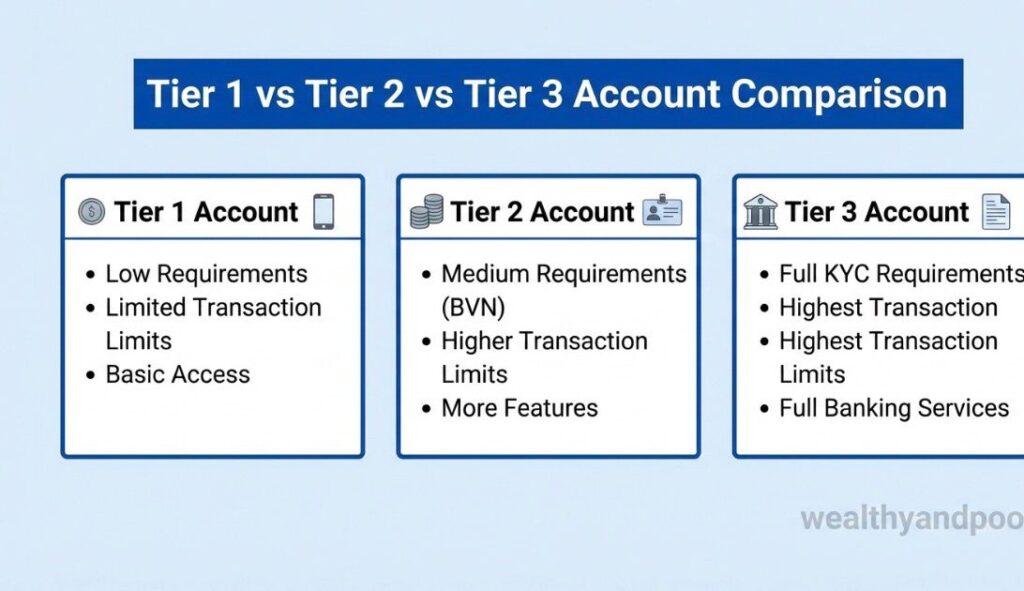

- Tier 1 Accounts The Entry Level :

Tier 1 accounts are usually the first step into formal banking. They are designed to be easy to open, even for people with limited documentation, like students, young adults, or first time account holders.

Key Features

- Minimal documentation: Often relies on basic personal info (name, phone number) and may not require full identity verification.

- Low transaction limits: Limits on deposits, transfers, and daily withdrawals are relatively low. For example, a typical Tier 1 account might allow a daily transfer of only ₦30,000 or a maximum balance of ₦300,000.

- Limited services: Some advanced banking services like international transfers or large loans may not be available.

Who It’s Best For

Tier 1 is ideal for people who:

- Are new to banking

- Don’t yet have full ID documents

- Want basic banking like saving

- small amounts or limited transfers

Tier 1 helps expand financial inclusion, letting more people participate in banking even before they complete full verification.

- Tier 2 Accounts The Middle Ground :

Once a customer provides more documentation such as a National Identification Number (NIN) or valid government ID a bank can upgrade a Tier 1 account to Tier 2.

Key Features.

- Moderate verification: Requires stronger ID but may not need proof of address.

-

Higher limits: Bigger transaction and balance limits than Tier 1 for example daily transfers up to ₦200,000-500,000 and a wider range of services.

-

More functionality: Tier 2 accounts typically support more banking features, such as mobile transfers, debit cards, and more consistent online access.

Who It’s Best For

Tier 2 suits:

- Salary earners

- Small business owners

- Freelancers and professionals

- People who need more flexibility but aren’t handling very large sums

This tier balances accessibility with increased financial capability.

- Tier 3 Accounts Full Access and High Limits:

To get a Tier 3 account, a customer usually must provide full documentation, including government issued ID and a proof of address (like a utility bill). This often involves a full “Know Your Customer” (KYC) verification process.

Key Features

- Highest limits: Daily transfers can reach ₦1,000,000 or more, and balance limits are high or even unlimited.

- Full functionality: Access to all banking services including large transfers, business banking tools, loans, and international services.

- Stronger compliance: Tier 3 accounts are fully compliant with anti-money-laundering and other regulatory checks.

Who It’s Best For

Tier 3 is tailored to:

- Business owners and entrepreneurs

- High-income earners

- Professionals handling large sums of money

- People who need full banking features and high transaction capabilities

This level gives users the widest range of services and capabilities.

Why Tiering Matters

Account tiers help banks:

- Combat fraud and money laundering

- Ensure compliance with financial regulations

- Provide appropriate service levels based on verification

- Protect customers (by limiting high-risk activity on minimally verified accounts)

For customers, understanding tiers means knowing what documentation is required and what features you’ll unlock as you move up.

Conclusion

In the end, the distinction between Tier 1, Tier 2, and Tier 3 accounts is not about hierarchy for its own sake, but about alignment matching account capabilities to real user needs, risk levels, and regulatory requirements.

Tier 1 accounts prioritize trust, security, and full functionality, making them the backbone for users who value stability, compliance, and unrestricted access.

Tier 2 accounts occupy a practical middle ground, offering expanded features while maintaining a balance between verification demands and usability.

Tier 3 accounts, by contrast, emphasize accessibility and speed, serving as an entry point for users who want to engage quickly with minimal commitment.

Understanding these tiers allows individuals and businesses to make informed decisions rather than default choices. The right tier is not necessarily the highest one available, but the one that supports your goals without unnecessary friction.

As platforms continue to refine their account structures, tiered systems will remain a strategic tool one that manages risk, enhances user experience, and scales services efficiently. Ultimately, knowing how these tiers differ empowers users to navigate platforms with confidence, clarity, and a sharper sense of control over how they participate in the digital ecosystem.

Comments